{kind=link}

I’ve had conversations with family and friends, and the query comes up, “The place ought to I put my cash [cash] to earn a protected yield. This comes from youthful folks beginning to construct a nest egg and older folks wanting to guard their nest egg. The choices requested about are excessive yield financial savings accounts, certificates of deposits (CDs), or paying off mortgages. One idea has confused folks when speaking about bond funds. There are two elements to mounted earnings return: 1) the yield, which is often paid day by day, month-to-month, quarterly, or yearly, and a couple of) modifications in yield that impression the worth of the bonds. If the yield goes down, the worth of the bonds appreciates. Collectively, yield and appreciation make up the entire return of the bond.

Danger comes within the type of period and the standard of the borrower. I’ve reviewed the chance of Lipper Bond Classes and segregated them loosely into three funding buckets for period and high quality risk-taking into consideration yield.

Notice that within the following tables, the metrics are from the previous three years, and I’ve elevated the yields of Municipal Bonds to be the equal of a taxable yield for somebody paying a marginal 22% tax charge.

Bucket Strategy

Christine Benz at Morningstar is a champion of the Bucket Technique. I’ll use her description from The Bucket Strategy to Constructing a Retirement Portfolio to explain the bucket technique.

The All-Necessary Bucket 1: The linchpin of any Bucket framework is a extremely liquid element to fulfill near-term dwelling bills for one yr or extra. Bucket 1 is under no circumstances a return engine, however the purpose of this portfolio sleeve is to stabilize the principal to fulfill earnings wants not coated by different earnings sources.

Bucket 2: Beneath my framework, this portfolio phase comprises 5 to eight years’ price of dwelling bills, with a purpose of earnings manufacturing and stability.

Bucket 3: The longest-term portion of the portfolio, Bucket 3 is dominated by shares and extra risky bond varieties, reminiscent of junk bonds.

Bucket #1: Security (Usually 1 to three Years)

I at the moment have about 18% of my funding in mounted earnings situated in Bucket #1. Bond funds which might be appropriate for Bucket #1 (Security) have each high-quality debt and brief period. I embrace short-duration funding grade bonds as a result of the chance of drawdown is comparatively low, however the yields are larger than Treasury payments. Over the previous three months, the highest 5 funds within the six Lipper Classes that I embrace in Bucket #1 have returned about 1 to 2% over the previous three months. I present the 5 funds that my Rating System charges the best.

Desk #1: Bond Bucket #1 for Security

Supply: Writer utilizing MFO Premium fund screener and Lipper international dataset; Morningstar for three-month return as of March twenty first

“Yield – Treasury” is a measure of how a lot additional yield the fund is paying in comparison with short-term Treasuries, that are thought of risk-free. “Yield/Ulcer” is a measure of how a lot threat the fund is taking for the yield that it pays. I restrict the worth to 10.

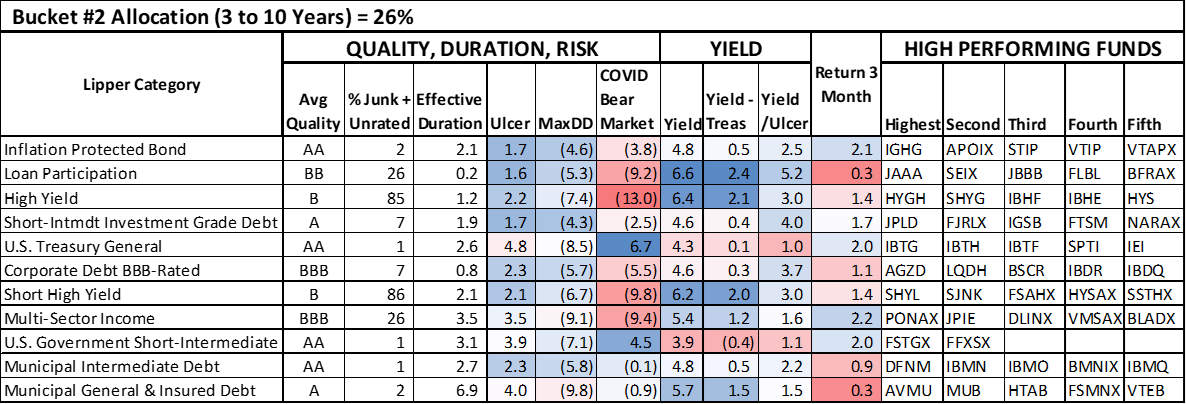

Bucket #2: Intermediate (Usually 3 to 10 Years)

Bucket #2 is essentially the most attention-grabbing to me as a result of dangers are reasonable as measured by the Ulcer Index, and yields are favorable. I’ve about 26% of my investments in mounted earnings allotted to Bucket #2 Lipper Classes, plus one other 18% in bond ladders.

The classes are ranked by Drawdown Danger, Bond High quality Danger, Period Danger, Yield, and Momentum. Inflation-Protected Bonds, Mortgage Participation, and Quick Period Excessive Yield are rated excessive. Protected authorities bonds have had the best return over the previous three months. I’ve been investing in excessive yield funds with brief durations and am monitoring efficiency.

Desk #2: Bond Bucket #2 – Intermediate Time Horizon

Supply: Writer utilizing MFO Premium fund screener and Lipper international dataset; Morningstar for three-month return as of March twenty first

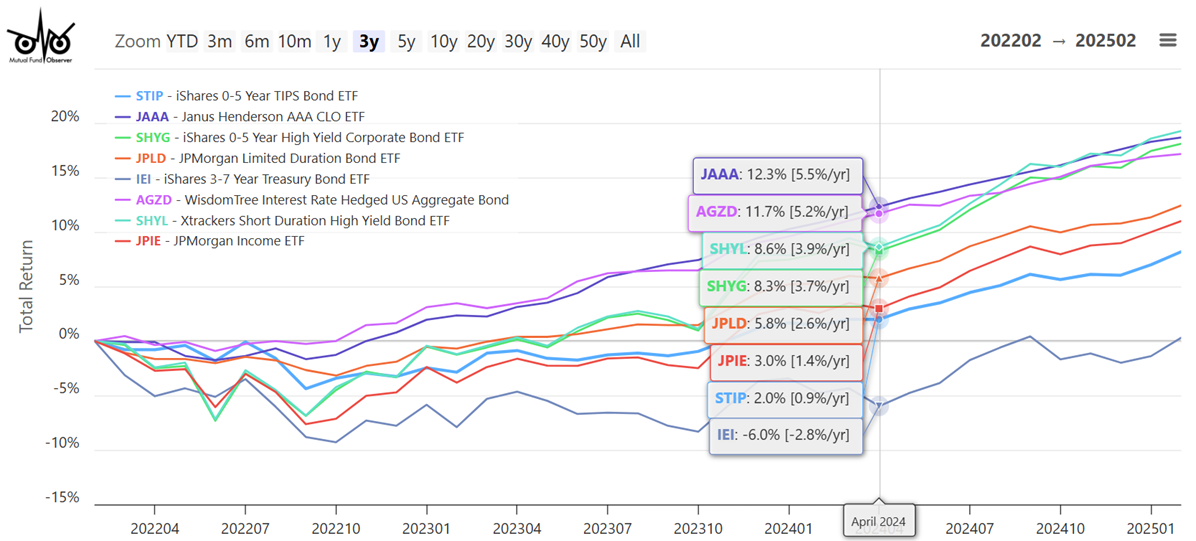

Determine #1: Efficiency of Chosen Funds from Bond Bucket #2

Supply: Writer utilizing MFO Premium fund screener and Lipper international dataset.

Bucket #3: Lengthy Time period (Usually 10+ Years)

I at the moment have about 39% of my investments in mounted earnings allotted to Bucket #3 Lipper Classes. I’m chubby in Conventional IRAs and take into account them to be in Bucket #2 due to required minimal distributions. A few of the bond classes in Bucket #3 seem in my extra aggressive Conventional IRA Bucket #2 sub-portfolios.

Bucket #3 comprises bond funds that will lose over ten % of their worth when charges are rising, as they did in 2022. The benefit of a number of the funds with larger high quality is that they’ve a low correlation to shares, so if shares are falling, the high-quality bonds sometimes rise.

Intermediate Authorities Bonds have excessive momentum now as yields on intermediate bonds have fallen. The period threat of those funds is excessive in order that the Ulcer Index, which measures the depth and period of drawdown, might be near that of the S&P 500 (Ulcer Index = 7.4). This emphasizes the significance of diversifying throughout classes.

Desk #3: Bond Bucket #3 – Lengthy Time period

Supply: Writer utilizing MFO Premium fund screener and Lipper international dataset; Morningstar for three-month return as of March twenty first

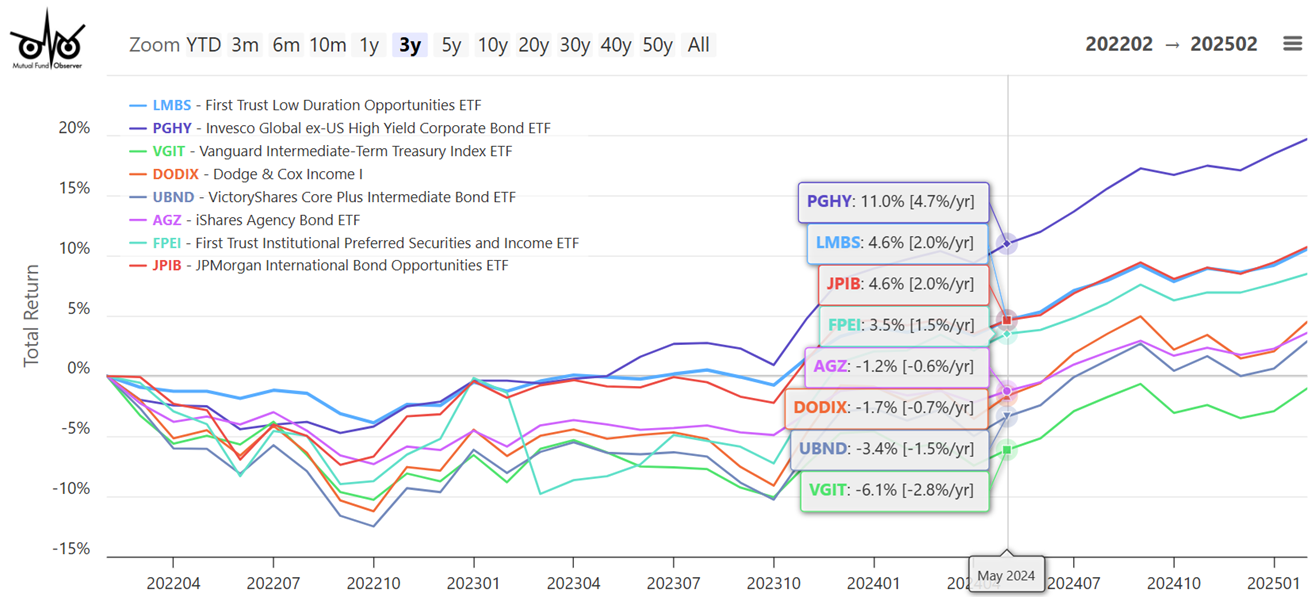

Determine #2: Efficiency of Chosen Funds from Bond Bucket #3

Supply: Writer utilizing MFO Premium fund screener and Lipper international dataset.

Closing

I’ve written a number of articles for Mutual Fund Observer as I transitioned into retirement virtually three years in the past. The three largest modifications have been 1) elevated reliance on the bucket technique, 2) switched from a complete return strategy to earnings technique in conservative Bucket #2 sub-portfolios to make the most of larger yields, and three) an elevated use of Monetary Advisors at Constancy and Vanguard to handle asset allocation, asset location, rebalancing, and tax effectivity in additional aggressive accounts.

Every month, I summarize the efficiency of funding buckets for the previous three months. Whereas maintaining turnover low to reduce taxes, if a fund stops performing the best way I anticipate, then I take into account changing it with one thing that appears to have longer-term potential. The above methods helped me sail by the latest correction with little impression or nervousness.

My present endeavor has been to summarize the taxes paid final yr on accounts and withdrawals. I plan to fulfill with my CPA this yr to debate tax effectivity and techniques. I started retirement planning over fifteen years in the past after I learn an inciteful ebook in regards to the impression of taxes on retirement withdrawals. Taxes shouldn’t be an after-thought in investing methods.