{kind=link}

Laptop Age Administration Providers Ltd – Main Registrar and Switch Agent for MFs

Included in 1988 and headquartered in Chennai, Laptop Age Administration Providers Ltd (CAMS) is India’s main and fastest-growing Certified Registrar and Switch Agent (QRTA) for Mutual Funds (MFs). With a market share of 68% based mostly on common asset below administration (AAUM), the corporate serves 10 out of 15 largest MF, together with the highest 4. The corporate additionally offers tech enabled monetary infrastructure and companies to numerous monetary establishments corresponding to asset administration firms (AMC), various funding funds (AIFs), and insurance coverage firms, fee & account aggregator and central file maintaining company for NPS. As of 31 December 2024, the corporate has a large bodily community comprising 286 service centres unfold throughout 25 states and 5 union territories.

Merchandise and Providers

CAMS presents numerous companies corresponding to MF RTA, digital onboarding companies; transaction processing, file administration, fund accounting and many others for AIF and PMS; insurance coverage repository companies; account aggregator for banks, NBFCs, funding advisors and many others; streamlining the NPS journey of consumers by means of eNPS registration, UPI-based checking account verification and many others; KYC registration company, RBI authorised fee aggregator, digital transformation, software program options and many others.

Subsidiaries: As of FY24, the corporate has 10 subsidiaries.

Funding Rationale

- Increasing market penetration – The corporate secured three MF-RTA mandates—Jio BlackRock MF, Pantomath MF, and Alternative MF. Moreover, it marked a major milestone by successful its first worldwide MF-RTA mandate from CeyBank AMC. CAMSREP, the corporate’s wholly owned subsidiary, has entered into an settlement with Life Insurance coverage Company of India (LIC) to offer insurance coverage repository companies. Moreover, CAMS has shaped a three way partnership with KFin Applied sciences Ltd. to collectively personal, develop, keep, and function the funding administration platform and ecosystem generally known as ‘MF Central’ (“Transaction”). Within the Alternate Funding Fund (AIF) phase, the corporate onboarded 21 new shoppers in Q3FY25. In its insurance coverage repository enterprise, the corporate secured a take care of Star Union Dai-ichi, making it the second life insurer to go for 100% policyholder protection with CAMS. On the insurance coverage aspect, it’s concentrating on a rise in insurance policies below administration from the present Rs.10 lakh to Rs.15 lakh per quarter.

- Robust operational efficiency – The corporate achieved its highest ever transaction quantity of Rs.24 crore (56% YoY progress) throughout Q3FY25. AUM grew 38% to Rs.46 trillion on the again of sturdy fairness belongings progress at 51%. Distinctive buyers grew by 31% to three.90 crore and Rs.0.98 crore new SIP registrations had been enrolled (a surge by 49% YoY), thereby growing the SIP e book to ~Rs.6 crore. Stay investor folio elevated by 35% throughout the quarter to Rs.9 crore accounts. These signify the corporate’s elevated income era potential, strengthened market management and wider investor base.

- Q3FY25 – Throughout Q3FY25, the corporate reported income of Rs.370 crore, a progress of 28% as in comparison with the Rs.290 crore of Q3FY24. That is backed by a 28% progress in MF income and 22% progress in non-MF income. EBITDA elevated by 34% from Rs.130 crore of Q3FY24 to Rs.174 crore of the present quarter. Internet revenue elevated from Rs.89 crore of Q3FY24 to Rs.125 crore of Q3FY25, a progress of 40% YoY. EBITDA margin improved from 45% to 47% and internet revenue margin elevated from 31% to 34% YoY.

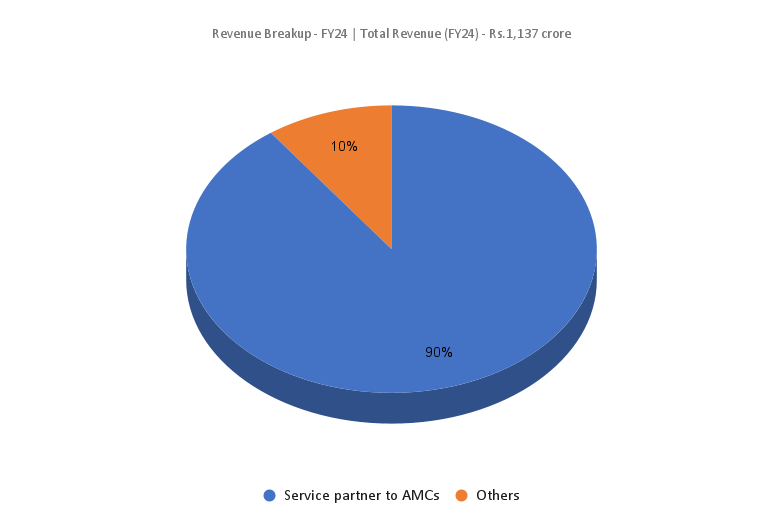

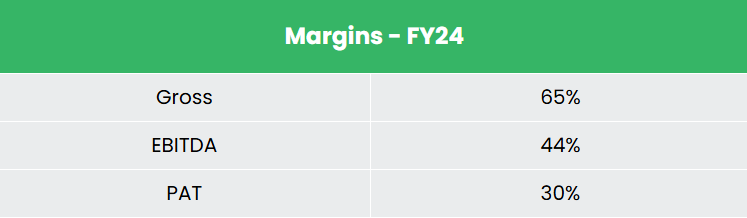

- FY24 – Speedy progress in transaction volumes and SIPs and buoyant investor confidence in capital markets has aided the corporate to generate a income of Rs.1,137 crore, a rise of 17% in comparison with the FY23 income. Working revenue is at Rs.505 crore, up by 20% YoY. The corporate reported internet revenue of Rs.354 crore, a rise of 24% YoY.

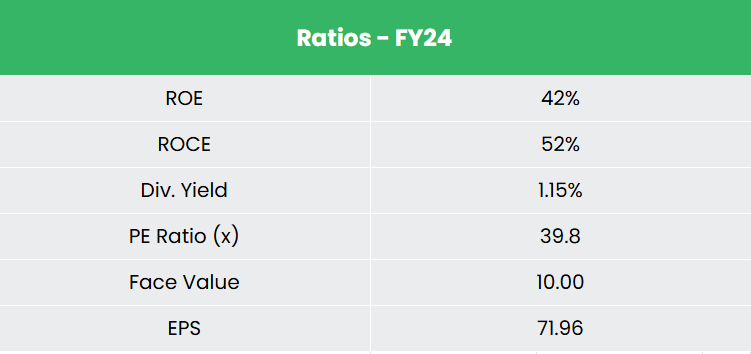

- Monetary Efficiency – The corporate has generated income and internet revenue CAGR of 17% and 25% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 41% and 50% for FY21-24 interval. The corporate has a debt-to-equity ratio of 0.09.

Trade

India’s monetary sector – which incorporates business banks, insurance coverage suppliers, non-banking monetary firms (NBFCs), cooperatives, pension funds, mutual funds, and different smaller monetary establishments – is witnessing speedy progress. This growth is pushed by each the sturdy efficiency of present companies and the entry of recent gamers into the market. With sturdy help from each the federal government and personal sector, together with the fast-paced adoption of cell and web applied sciences, India is rising as one of many world’s largest digital markets. As of FY25 (as much as January 2025), the mutual fund trade’s Property Below Administration (AUM) reached Rs.68.05 lakh crore (US$ 789.44 billion). Throughout the identical interval, investments by means of Systematic Funding Plans (SIPs) totalled Rs.2,37,427 crore (US$ 27.54 billion).

Progress Drivers

- Decrease mutual fund penetration of 5-6% displays latent progress alternatives given the rise of salaried middle-class inhabitants.

- The Union Funds 2025 has introduced a rise of FDI sectoral cap for the insurance coverage sector from 74% to 100%. This enhanced restrict can be accessible for these firms, which make investments the complete premium in India.

- The discount within the tax burden within the 2025-26 Union Funds is anticipated to spice up the investable quantity accessible among the many increasing center class inhabitants.

Peer Evaluation

Competitor – KFin Applied sciences Ltd.

In comparison with its competitor, the corporate is producing higher returns from invested capital aided by a steady progress in income, indicating its prudent capital allocation and income producing capabilities.

Outlook

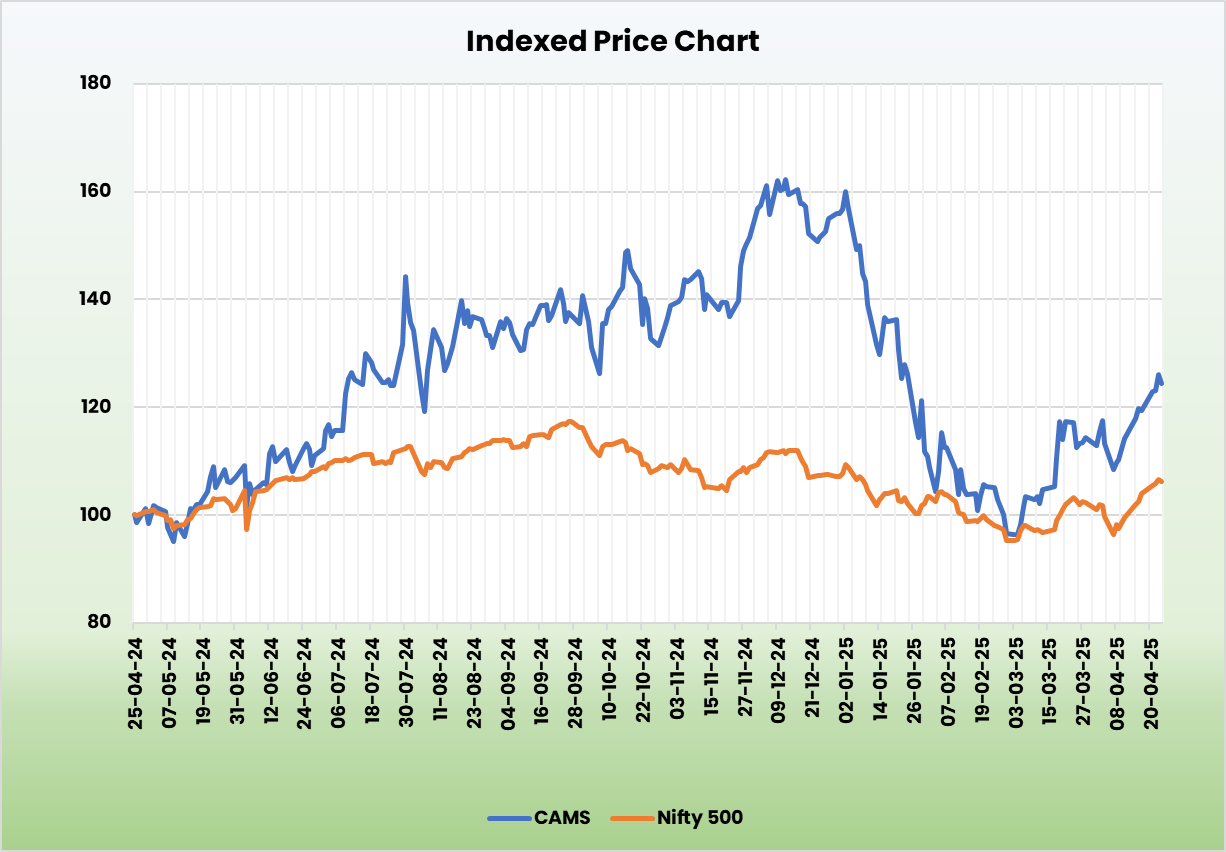

With a market share of ~68% based mostly on AAUM, 62% share in new SIP registration and 70% share of NFO assortment, CAMS has marked its place as a key monetary middleman within the Indian capital market. Its cutting-edge IT platforms and cell purposes have enabled the corporate in offering superior expertise options to its prospects. Notably the corporate is securing an growing variety of inbound contracts from each home and worldwide shoppers.

Valuation

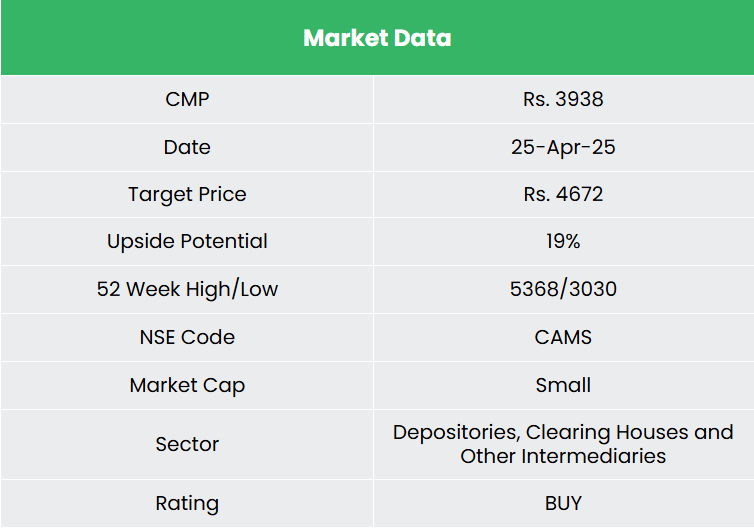

Being the market chief QRTA in India’s quick rising mutual fund trade, strongly backed by the federal government’s impetus on digital transformation of economic companies, we imagine CAMS is nicely positioned to speed up its progress momentum. We advocate a BUY ranking within the inventory with the goal worth (TP) of Rs.4,672, 48x FY26E EPS.

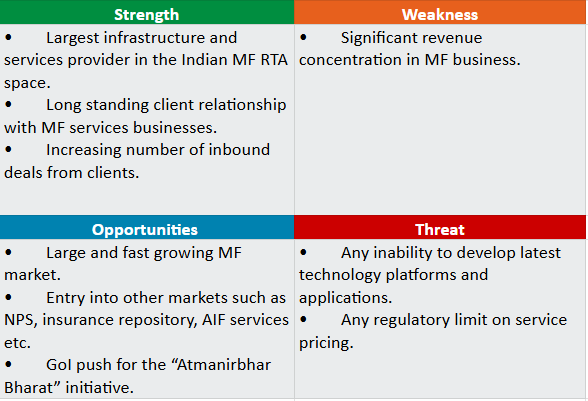

SWOT Evaluation

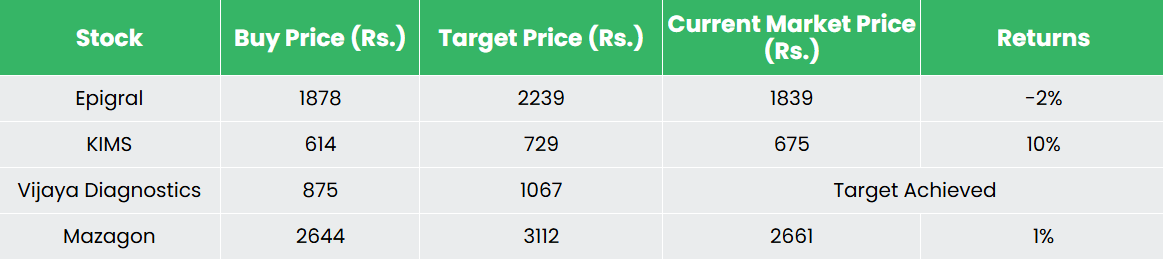

Recap of our earlier suggestions (As on 25 April 2025)

Krishna Institute of Medical Sciences Ltd

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM on no account assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like

Put up Views:

162