{kind=link}

In yesterday’s put up, we concluded that rates of interest had been influenced—however not set—by the Fed. We additionally noticed that charges had been influenced—however not set—by the availability and demand of capital. We famous in each circumstances, nonetheless, that there was appreciable variance over what these two fashions indicated, which suggests there’s something else occurring.

To determine what that “one thing else” is, I need to dig a bit deeper into the charges themselves. In principle, charges encompass three components: a foundational risk-free fee, which is what traders must postpone present consumption; plus compensation for credit score danger; plus compensation for inflation danger. If we use U.S. Treasury charges as the premise for our evaluation, we will exclude credit score danger (sure, I do know, however work with me right here) and are left with the risk-free fee plus inflation.

U.S. Treasury Fee

The chart under reveals that relationship, with charges extremely correlated with inflation. Nevertheless it additionally reveals one thing completely different: past the drop in inflation, there was one thing else taking place to deliver rates of interest as little as they’re. The danger-free fee, which is the hole between the 10-year Treasury fee and the inflation fee, has declined as properly.

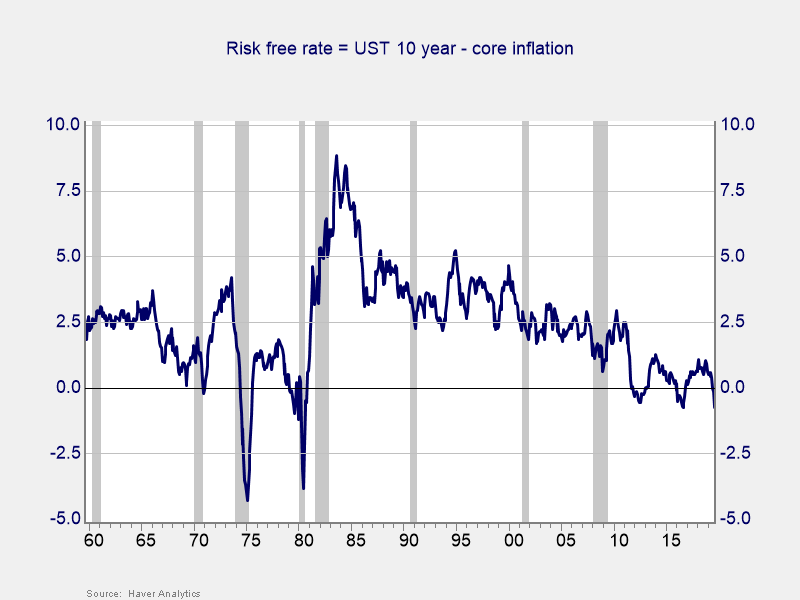

Threat-Free Fee

We are able to see that decline clearly within the chart under, which reveals the risk-free fee, calculated because the 10-year Treasury fee much less core inflation. From the early Eighties to the early 2010s, that fee declined steadily. Whereas inflation went up and down and geopolitical occasions got here and went, there was a gentle lower in what traders thought-about to be a base stage of return. Lately, that risk-free fee has held pretty regular at round zero.

Any rationalization for this conduct has to account for each the multidecade decline and the current stabilization round zero. It additionally has to account for the truth that we have now been right here earlier than. By analyzing charges on this manner, we will see that present situations aren’t distinctive. We noticed one thing comparable within the late Sixties by way of Nineteen Seventies.

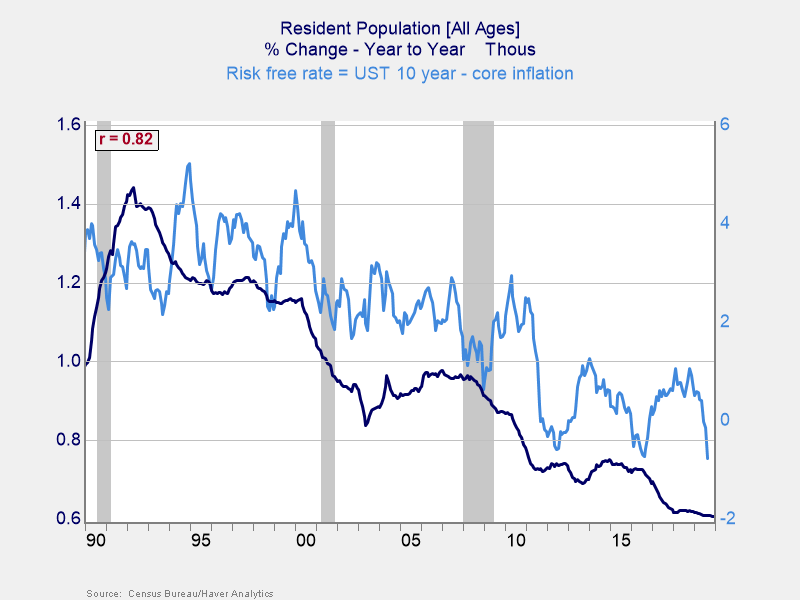

Inhabitants Progress

There aren’t too many elements which have a constant pattern over many years, which is what is required to clarify this sort of conduct. There are additionally few elements that function at a base stage to have an effect on the economic system. The one one that matches the invoice, in truth, is inhabitants development. So, let’s see how that works as a proof.

Because the chart reveals, inhabitants (particularly, development in inhabitants) works very properly. From 1990 to the current, slowing inhabitants development has gone hand in hand with decrease risk-free charges. Empirically, the information is strong, however it additionally makes theoretical sense. Youthful populations are inclined to develop extra shortly, whereas older ones develop extra slowly. A rising inhabitants wants extra capital, to construct houses, companies, and so forth. However slower development depresses the demand for capital.

This mannequin incorporates each the Fed and market fashions, however it provides them a extra strong basis. It additionally explains why charges have remained low just lately, regardless of each the Fed and market fashions signaling they need to rise. With inhabitants development low and prone to keep that manner, there’ll proceed to be an anchor on charges going ahead.

This mannequin additionally gives a solution to certainly one of our earlier questions, as to why charges within the U.S. are increased than in Europe and why European charges are increased than in Japan. Taking a look at relative inhabitants development, this state of affairs is precisely what we must always see—and we do. If we take into account when charges began trending down in Europe and Japan, we additionally see that the timelines coincide with slowdowns in inhabitants development. Few issues are ever confirmed in economics, however the circumstantial proof, over many years and across the globe, is compelling. Low inhabitants development results in low risk-free rates of interest.

The Reply to Our Query

Charges are low as a result of inhabitants development is low. Charges are decrease elsewhere as a result of inhabitants development is even decrease. This case shouldn’t be going to alter over the foreseeable future, so we will anticipate decrease charges to persist as properly. This reply nonetheless leaves the query of inflation open, in fact, however that’s one thing we will look ahead to individually. The underlying pattern will stay of low charges. And that basically is completely different—if not from historical past, as we noticed above, a minimum of from most expectations.

As you would possibly anticipate, this rationalization has fascinating implications for each financial coverage and our investments. We’ll end up subsequent week by these subjects.

Editor’s Notice: The unique model of this text appeared on the Impartial Market Observer.