| Mutual Fund Observer")

{kind=link}

THIS IS AN UPDATE OF THE FUND PROFILES revealed in 2009 and 2013.

Goal and technique

The fund seeks long-term capital appreciation by investing in a diversified portfolio of very, very small North American corporations.

Aegis believes extra returns will be generated by:

- buying a well-researched portfolio of essentially sound small-cap shares buying and selling at low valuations during times of stress or neglect, when liquidity is low and investor sentiment is poor,

- holding these investments patiently by way of intervals of short-term value volatility whereas elementary circumstances normalize, and

- promoting after elementary traits reverse, as restoration turns into seen and investor sentiment improves, driving valuations greater.

They search for shares which are “considerably undervalued,” given elementary accounting measures together with e-book worth, revenues, or money circulate. They outline themselves as “deep worth traders.” Whereas the fund invests predominantly in microcap shares, it does have the authority to put money into an all-cap portfolio if that ever appears prudent.

Adviser

Aegis Monetary Company of McLean, Virginia, is the Fund’s funding advisor. Aegis has been in operation since 1994 and has suggested the fund since its inception in 1998.

Supervisor

Scott L. Barbee, CFA, is portfolio supervisor of the fund and a Managing Director of AFC. He was a founding director and officer of the fund and has been its supervisor since inception. He additionally manages 66 separate fairness account portfolios of different AFC shoppers managed in an funding technique just like the Fund, with a complete worth of roughly $30 million. Mr. Barbee obtained an MBA diploma from the Wharton Faculty on the College of Pennsylvania. He’s supported by 4 different professionals.

Technique capability and closure

Aegis Worth closed to new traders in late 2004, when property within the fund reached $820 million. The supervisor estimates that, beneath present circumstances, the technique may accommodate roughly $1.5 billion. That aligns with the dimensions of its common holding.

Administration’s stake within the fund

As of June 2025, Aegis workers owned greater than $48 million of Fund shares. The overwhelming majority of that funding is held by Mr. Barbee and his household. Two of the fund’s three unbiased administrators, although very modestly compensated, have giant stakes within the fund.

Opening date

Could 15, 1998

Minimal funding

Nominally $10,000 for normal accounts and $5,000 for retirement accounts, however brokerages similar to Schwab require a $1 minimal preliminary funding.

Expense ratio

1.45% on property of $560 million, as of June 2025. The fund has attracted about $100 million in inflows within the first half of 2025. With a administration price of 1.2%, room for extra expense reductions is modest.

Feedback

Small-cap worth investing has lengthy been out of favor as traders feverishly choose themselves on what number of FAANGs or MAGs they’ve managed to accumulate. Aegis Worth presents the case for double-checking these simple impulses. My colleague, Devesh Shah, engaged in an extended dialog with Mr. Barbee in 2023, which resulted within the essay, “In Dialog with Scott Barbee, Portfolio Supervisor at Aegis Worth Fund” (8/2023). Devesh and Scott talked at size about his investable universe and his (since validated) notion of “a uncommon and engaging alternative” which now dominates his portfolio. Given the depth of these discussions, this profile will restrict itself to a few arguments: (1) Aegis is outstandingly profitable, (2) Aegis is distinctive, and (3) the Aegis self-discipline is sensible.

1. Aegis is outstandingly profitable

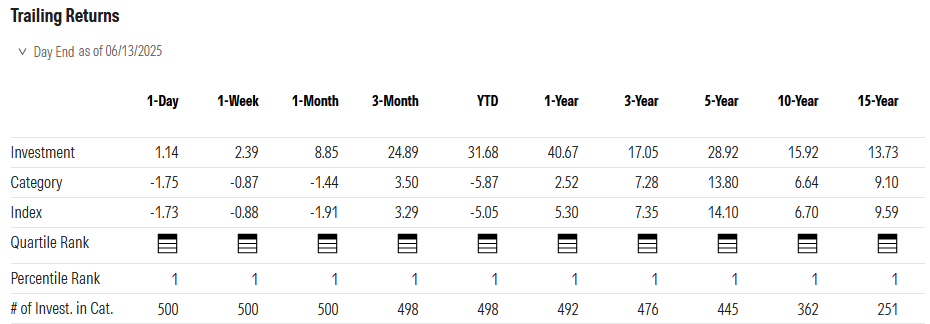

As we composed this profile in mid-June 2025, Morningstar reported the next absolute and relative returns for Aegis Worth. We should always take a look at each the row labeled “Funding” and the one labeled “Percentile Rank.” The primary row signifies annualized returns over quite a lot of trailing intervals; as an example, the fund has averaged a return of 13.73% yearly for the previous 15 years. The decrease row reveals how that ranked inside its peer group. The “1” implies that Aegis Worth was within the high 1% of its friends over the previous 15 years.

Supply: Morningstar.com, 6/14/2025

The highest 1% over the previous 15 years is outstanding. The highest 1% over the previous week, month, quarter, yr, three years, 5 years, ten years, and 15 years is just about unprecedented. It’s additionally not a fluke: Lipper gave Aegis a five-star ranking for consistency over the lifetime of the fund, the identical ranking assigned by MFO Premium’s calculation of the fund’s Ferguson Consistency Index: Lifetime.

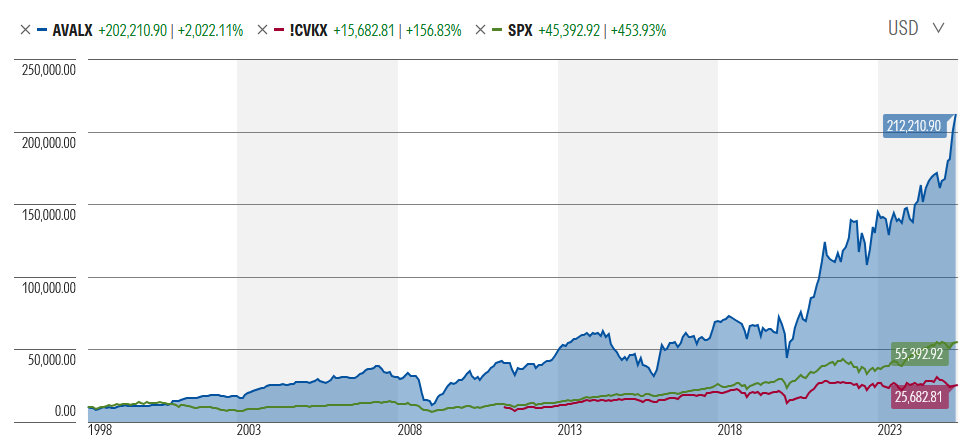

The fund has achieved properly even compared to its antithesis: the large-cap growth-oriented S&P 500. A $10,000 funding in Aegis at inception has grown to $202,000 at present; the identical funding within the S&P 500 has risen by one-fourth as a lot.

Supply: Morningstar.com, 6/14/2025

2. Aegis is distinctive.

It’s now, because it has continuously been, a portfolio incomparable to friends or benchmarks. Energetic Share measures the independence of a portfolio from its benchmark; the upper the energetic share, the larger the distinction and the larger the prospect that the returns symbolize a supervisor’s talent fairly than his asset class’s successor. Aegis has an Energetic Share of 99.3%, the very best of any fund we monitor. In 2022, we constructed a basket of small-cap worth funds with the very best high quality portfolios (up to date this month in “Extra soiled intercourse and your spanked portfolio: A 3-year assessment,” 7/2025). Of the 11 funds – energetic and passive – in that basket, Aegis had the bottom correlation to its peer group, to its benchmark, and to the S&P 500.

Concrete markers of that distinction come from a look on the portfolio:

- 92% of the portfolio is in simply two sectors: supplies and power. The peer weight is 11%.

- 15% of the portfolio is within the US, in comparison with 97% for friends

- 59% of the portfolio is invested in Canada accounting versus 1% for friends.

- 42% is invested in microcap shares, in comparison with 9% for its friends

- By Morningstar’s metrics, the fund’s common market cap is $655 million, the typical holding in its friends is 800% bigger

- The fund at present holds 9% money, in comparison with 1.7% for friends (and 4% two years in the past, when Devesh spoke with Mr. Barbee).

That offers some weight to a remark that Mr. Barbee made to Devesh in 2023: “We’re an odd duck in that we do detailed work on shares as if we have been a hedge fund with out charging the efficiency charges.”

3. The Aegis self-discipline is sensible.

Many managers declare to disregard macroeconomic elements. “We’re not into political economics. We simply purchase the perfect shares obtainable” is their mantra. Mr. Barbee appears to have fairly extra sympathy for understanding Massive Image points than attempting to place Aegis Worth for fulfillment inside them. There appear to be two massive image points on his thoughts. First, the foremost US inventory indices are extremely concentrated and wildly overvalued:

At this time, speculative fervor continues to dominate the markets. The ratio of property in levered lengthy ETFs to property briefly ETFs hit 11.1 occasions, probably the most on file in keeping with Bloomberg. Fund Supervisor Survey money allocations are on the lowest since 2001 in keeping with Financial institution of America. Retail sentiment can be unusually sturdy with Households all-in on equities. Ned Davis Analysis just lately reported that shares as a share of whole family monetary property hit 36.1 p.c, the very best family allocation to equities since 1952. NYSE margin debt can be on the rise, climbing almost 50 p.c within the final two years to ranges close to $900 billion at present. US equities at present are top-heavy, fully-valued, and weak to say no. The market capitalization of the top-10 shares within the S&P 500 Index at year-end constituted almost 40 p.c of the general index, with the biggest market-cap inventory at a file valuation 750 occasions as giant because the seventy fifth percentile inventory within the Index, a focus degree not seen because the Nineteen Thirties, in keeping with Goldman Sachs. (Shareholder Letter, 1/27/2025)

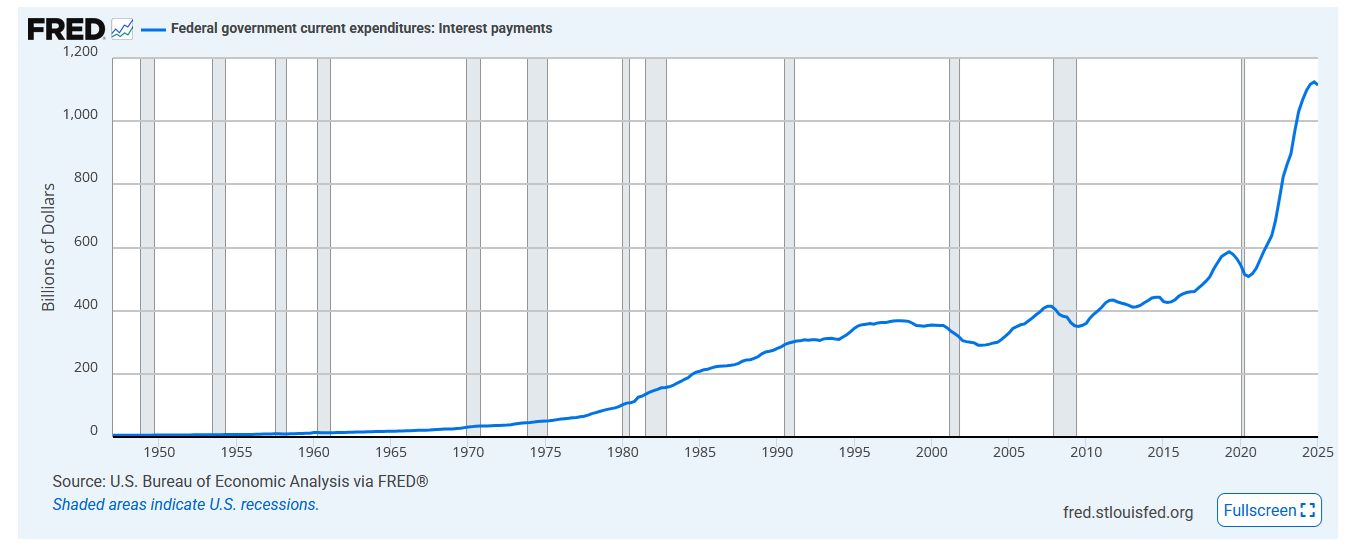

Second, the federal authorities’s lack of ability to align its revenue with its bills dangers resulting in a debasement of the greenback. The federal authorities’s standing because the world’s most secure funding and strongest haven is being known as into query by a debt that’s so giant that curiosity funds on it exceed $1 trillion a yr.

Supply: St. Louis Fed, 5/29/2025

Debt funds are the third-largest, and the fastest-growing, class of federal outlay. The mixture of giant deficits and diffidence from worldwide traders creates the prospect for actual and sustained inflation. As DoubleLine founder and hedge fund supervisor Jeff Gundlach warned in June: “a reckoning is coming.”

Mr. Barbee believes that he has positioned the portfolio intelligently in gentle of each of these elements.

We consider our angular portfolio, with a powerful concentrate on supplies and power, is properly positioned given at present’s surroundings We’re at present sustaining a portfolio that’s unusually angular, with excessive focus amongst quite a lot of deeply undervalued small-cap power and supplies shares from the worth universe, together with a considerable variety of Canadian shares and some different international equities. Many of those Fund positions have been performing properly regardless of the numerous headwinds of a quickly strengthening greenback. Nevertheless, with the greenback hitting new highs, sentiment in the direction of securities buying and selling exterior the USA has deteriorated markedly. Resultingly, considerably decrease valuations stay obtainable on international securities. With the sturdy greenback now trying fairly prolonged, and with US expertise equities at present within the highlight, we consider it’s a nice time to be opportunistically positioned in worldwide, commodity-producing shares, notably provided that commodities are usually priced in {dollars}. Ought to the greenback roll-over, whether or not pushed by a brand new Washington political consensus or in any other case, the current greenback headwinds confronted by worldwide shares and commodity producers may quickly shift to tailwinds. Because the S&P 500 has soared in the previous couple of years, US small caps have additionally been underperforming, with many managers showing to be dropping by the wayside. Fund supervisor positioning towards small-cap shares was just lately reported by Financial institution of America to be on the lowest degree in information going again to 2015. (Shareholder Letter, 1/27/2025)

The portfolio is positioned to learn from declines within the US greenback, and plenty of of its holdings are thought-about conventional inflation hedges.

Backside Line

Aegis Worth is a deep-value fund that has historically discovered a few of the most compelling values within the small- to microcap area. Mr. Barbee is without doubt one of the subject’s longest tenured managers, and Aegis sports activities one among its longest information. Each testify to the truth that steadfast traders right here have had their endurance greater than adequately rewarded. It’s best to think about it.

Fund web site

Aegis Worth fund. We’d principally commend the wealth of shareholder letters to you.