{kind=link}

Epigral Ltd – India’s Main Built-in Chemical Producer

Based in 2007 and headquartered in Ahmedabad, Epigral Ltd. (previously Meghmani Finechem Ltd.) is a pacesetter in India’s chemical business. Beginning with Chlor-Alkali manufacturing in Dahej, the corporate has expanded to incorporate Chloromethanes, Hydrogen Peroxide, Epichlorohydrin, and CPVC. It has India’s first Epichlorohydrin plant based mostly on renewable sources and the most important CPVC plant, driving nation’s infrastructure progress. Their cutting-edge manufacturing facility spans 60 hectares in Dahej, Gujarat.

Merchandise and Providers

Epigral affords a variety of important derivatives and specialty chemical substances throughout 15+ industries:

- Chlor-Alkali: Merchandise like caustic soda, caustic potash, liquid chlorine, and hydrogen fuel, utilized in alumina, textiles, chemical substances, soaps, detergents, agrochemicals, and prescribed drugs.

- By-product Merchandise: Contains chloromethanes and hydrogen peroxide, serving the pharmaceutical, PTFE pipes, refrigerant fuel, paper and pulp, textile, chemical, and effluent therapy industries.

- Specialty Chemical substances: CPVC resin, CPVC compound, epichlorohydrin (ECH), and chlorotoluene worth chain, utilized in pipes and fittings, windmills, cars, adhesives, agrichemicals, and APIs.

Subsidiaries: As of FY24, the corporate has one affiliate firm.

Development Methods

- Capability Growth: Throughout Q1FY25, Epigral elevated CPVC resin capability by 45,000 TPA, reaching 75,000 TPA. It additionally added 35,000 TPA in CPVC compounds through the quarter.

- New Ventures: Increasing into chlorotoluene and its worth chain for pharmaceutical and agrochemical intermediates, with commissioning anticipated by Q2FY25.

- R&D Enhancement: Launched a Analysis and Improvement Centre in Ahmedabad in FY24 to spice up specialty product innovation.

- Capability Utilization: Optimum utilization of latest services is projected from FY26.

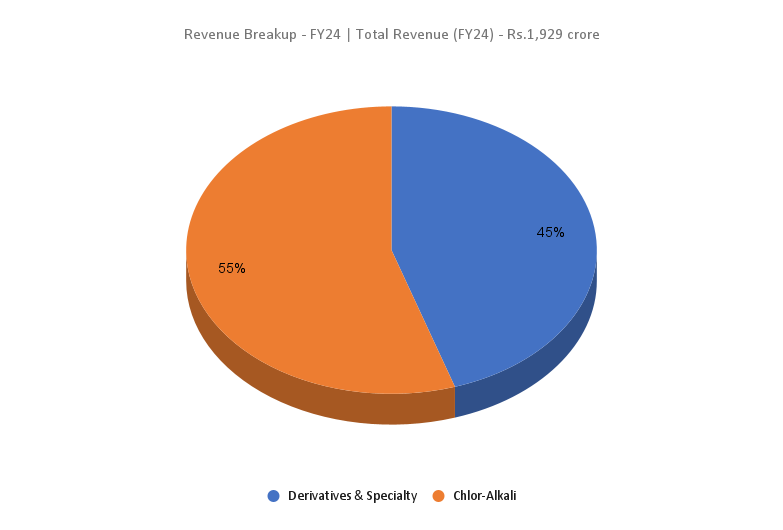

- Product Combine Shift: Aiming to shift the product combine from 45:55 to 70:30, favoring derivatives and specialty chemical substances over chlor-alkali.

- Market Management: Holds high nationwide capacities in caustic soda, caustic potash, chloromethanes, hydrogen peroxide, CPVC resin, and India’s first ECH plant.

Monetary Efficiency

Q1FY25

- Income reached ₹654 crore, up 43% YoY.

- Quantity grew 29%, led by Derivatives and Specialty enterprise.

- EBITDA elevated 85% to ₹176 crore.

- Internet revenue jumped 169% to ₹86 crore.

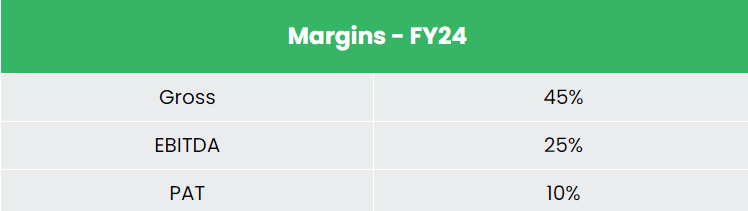

- Margins improved: gross margin to 40%, EBITDA margin to 27%, and web revenue margin to 13%.

- Product realization declined regardless of sturdy progress.

FY24

- Quantity grew 15%, boosted by diversification and new tasks.

- Income declined 12% to ₹1,929 crore attributable to decrease realizations.

- Working revenue fell 30% to ₹481 crore, and web revenue dropped 44% to ₹196 crore.

- Business confronted subdued demand, oversupply, and low realizations.

Monetary Efficiency (FY21-24)

- 3-year income and PAT CAGR: 33% and 25% (FY21-FY24).

- 3-year common ROE: 30%, ROCE: 26%.

- Wholesome capital construction with a debt-to-equity ratio of 0.77.

Business outlook

- India’s chemical business covers over 80,000 merchandise, together with bulk chemical substances, specialty chemical substances, agrochemicals, petrochemicals, polymers, and fertilizers.

- The business is the sixth largest globally and third largest in Asia.

- Regardless of challenges like inflation and provide chain disruptions, the sector has proven resilience.

- Projected progress: $300 billion by 2025 and $1 trillion by 2040.

- India ranks eleventh in chemical exports and sixth in imports (excluding prescribed drugs).

Development Drivers

- Authorities allotted ₹192.21 crore (US$ 23.13 million) to the Division of Chemical substances and Petrochemicals below the Interim Union Finances 2024-25.

- A 2034 imaginative and prescient has been established to spice up home manufacturing, scale back imports, and appeal to investments within the chemical substances and petrochemicals sector.

- 100% FDI is permitted below the automated route, with some exceptions for hazardous chemical substances.

Aggressive Benefit

Epigral displays superior gross sales progress and more healthy returns on investments in comparison with rivals like Grasim Industries Ltd and DCM Shriram Ltd.

This efficiency highlights Epigral’s prudent capital allocation and increasing market penetration.

Outlook

- Epigral’s shift from fundamental chemical substances to specialised merchandise, a primary in India technique, is about to place the corporate as a key chief available in the market.

- By transitioning to area of interest Derivatives and Specialty chemical substances, Epigral is anticipated to be much less affected by market fluctuations.

- With sturdy earnings progress potential and underutilized just lately commissioned capacities, the corporate is well-positioned for important future progress and worth creation.

Valuation

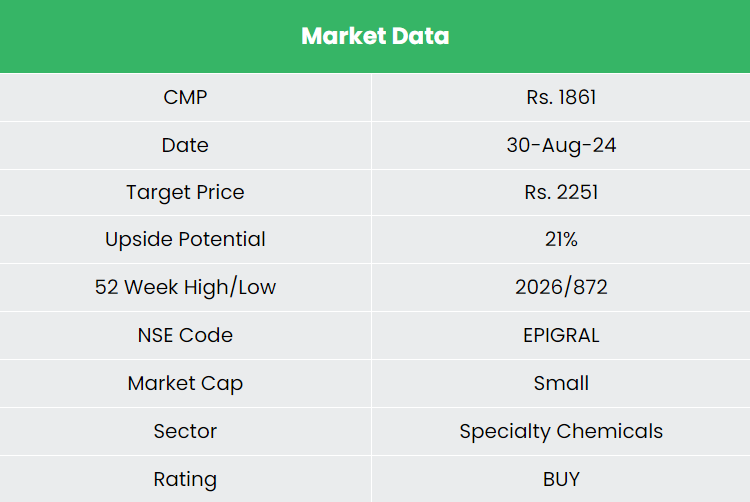

Epigral’s technique to develop Derivatives and deal with import substitution is anticipated to drive progress. Introducing “India’s first” merchandise will additional improve its market place. We advocate a BUY score with a goal worth (TP) of ₹2,251, based mostly on 27x FY26E EPS.

Dangers

- Single Manufacturing Unit: All manufacturing and capability expansions are concentrated at a single location in Dahej, posing dangers if any sudden points come up on the website.

- Demand Slowdown: A decline in demand in home or export markets may negatively impression margins.

Notice: Please word that this isn’t a advice and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

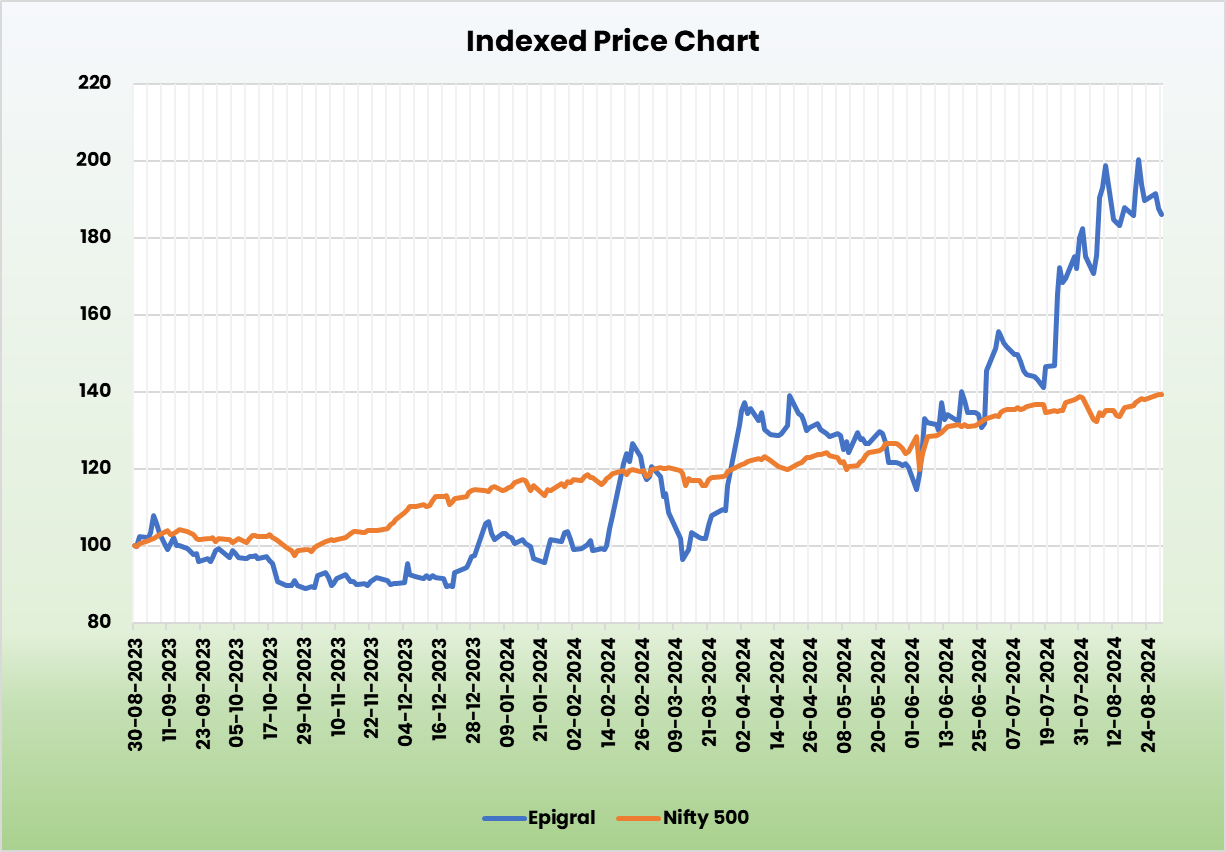

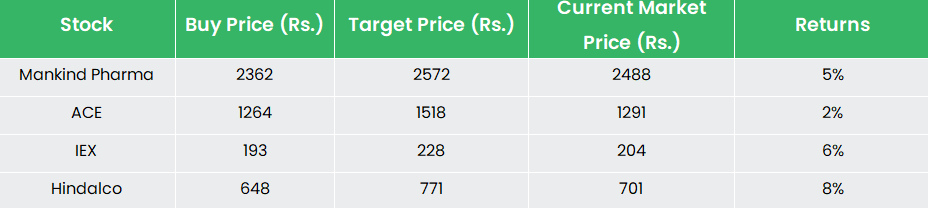

Recap of our earlier suggestions (As on 30 August 2024)

Different articles you could like

Submit Views:

1,092