{kind=link}

Historically, the job description for a core bond supervisor was numbing: (1) present up for work, (2) purchase a bunch of Treasury bonds and a few funding grade intermediate corporates, (3) have a good time the buying and selling coup that allowed you to purchase the identical bond as everybody else however for 1 / 4 foundation level much less – woohoo!, (4) go house and revel in a fiber-rich dinner and small glass of purple wine.

In actuality, managers added negligible worth. Over 10 years (via August 2025), the core bond fund trailing 75% of its friends returned 1.7% yearly, the iShares Core US Combination Bond ETF (a proxy for “the market”) returned 1.8% yearly, and a fund main 75% of its friends returned 2.2%. Internet distinction between cellar and penthouse: 0.5% per yr. (Supply: MFOPremium calculations, Lipper International Datafeed knowledge.) And that’s fairly typical for different trailing intervals. Because of this, relative returns had been extremely depending on effectivity: very giant funds with very low expense ratios, capable of place bids on very giant numerous very effectively priced bonds, had a virtually unbeatable structural benefit.

Cellar versus penthouse

10-year efficiency distinction between

the highest quartile and the underside quartile

Core bond: 0.5% yearly (per MFO Premium)

Core inventory: 1.6% yearly (per Morningstar)

In a world the place US Treasury bonds are the world’s most secure funding and amongst its most reliably worthwhile, it was an unbeatable recipe.

We is perhaps leaving that world behind, which suggests we would want to think about prospects the place diversification and supervisor judgment would possibly add substantial worth.

That means the potential for contemplating an ongoing stake in credit score quite than simply funding grade, in worldwide quite than simply U.S., in particular conditions quite than simply vanilla auctions, and in shorter durations.

The case for trying broadly

For clever buyers—no matter whether or not monetary evaluation is a every day behavior or a distant curiosity—it’s changing into more and more troublesome to disregard the mounting alarm bells surrounding america’ fiscal outlook. In mid-2025, the nationwide debt stands at over $37 trillion, a sum now better than your complete American financial system. This staggering determine displays years of price range deficits and a political local weather the place coverage selections usually seem pushed extra by ideology, self-interest and brinkmanship than any rational financial technique. Even main buyers, as soon as reliant on U.S. Treasury bonds for safety, are starting to query how for much longer the world’s largest borrower can sustainably fund its wants with out consequence (Drew Desilver, “Key info in regards to the US nationwide debt,” Pew Analysis, 8/12/2025).

| Nationwide debt earlier than the Reagan Revolution (1980) | $900 billion 32% of GDP |

| Nationwide debt (2025) | $37.4 trillion 120% of GDP |

(Sources: Historic Debt Excellent, US Treasury; Federal Reserve Financial institution of St Louis, 9/2025)

These fiscal realities should not occurring in isolation. Because the U.S. authorities takes on extra debt, with rising prices simply to pay curiosity, confidence in federal bonds has begun to erode. Latest episodes of political gridlock over spending caps and the debt restrict have highlighted simply how reactive and unpredictable U.S. fiscal coverage has grow to be. The sensible impact is a brand new period of vulnerability for conventional revenue portfolios anchored virtually solely on U.S. Treasuries and investment-grade corporates. Traders are seeing the worth of home-country property more and more formed by fiscal danger and short-term fixes quite than predictable financial fundamentals.

In distinction, a rising variety of international markets not solely boast extra engaging valuations but additionally sign ripening alternatives as non-U.S. economies chart their very own paths out of stagnation. Diversification, due to this fact, isn’t merely about chasing greater yields or speculating overseas—it’s rising as a crucial hedge towards the potential excesses of U.S.-centric fiscal and market dynamics.

One measure of that modified dynamic is Analysis Associates’ estimates of the dangers and returns, given a sequence of uniform financial assumptions, of dozens of asset lessons. The next desk offers the ten highest Sharpe property plus the US bond combination. Classes in black are mounted revenue (seven of 11), and blue are fairness.

(Supply: Analysis Associates, Asset Allocation Interactive, 9/2025)

In contrast, the three asset lessons with detrimental anticipated 10-year Sharpe ratios are US Massive-Cap shares (-0.03), Developed Markets Massive Development shares (-0.06), and US Massive Development shares (-0.12).

Backside line: buyers want to think about searching for core publicity, not simply 5% nibbles, in areas past the frequent.

Earnings past the unusual

The unhealthy information is that lots of the most intriguing revenue investments should not simply accessible to most buyers: closed-end interval funds resembling RBC Blue Ray Destra Worldwide Occasion-Pushed Credit score (CEDIX) or Carlyle Tactical Personal Credit score (TAKNX), usually have excessive minimums and restricted brokerage entry. Others, resembling SEI Opportunistic Earnings (SIIT) Fund and GMO Rising Nation Debt, are institutional. These structural quirks – the flexibility to make use of leverage and to lock giant investments in place by denying buyers the prospect to redeem at will – give these managers distinctive benefits.

That mentioned, there are intriguing choices out there to common buyers. We searched the MFO Premium database for funds that met six standards:

- They’d a file of 5 years or extra.

- They had been income-oriented.

- They might make investments globally and throughout asset lessons.

- They returned a minimum of 4% yearly. By comparability, the Vanguard Complete Bond Market Index has misplaced 0.8% yearly over the previous 5 years.

- They moved independently of the US bond market (draw back seize of lower than 50%, correlation of lower than 75%).

- They earned the MFO Nice Owl designation (funds will need to have high 20% risk-adjusted returns for all of the trailing measurement intervals).

And, lastly, they needed to be purchasable.

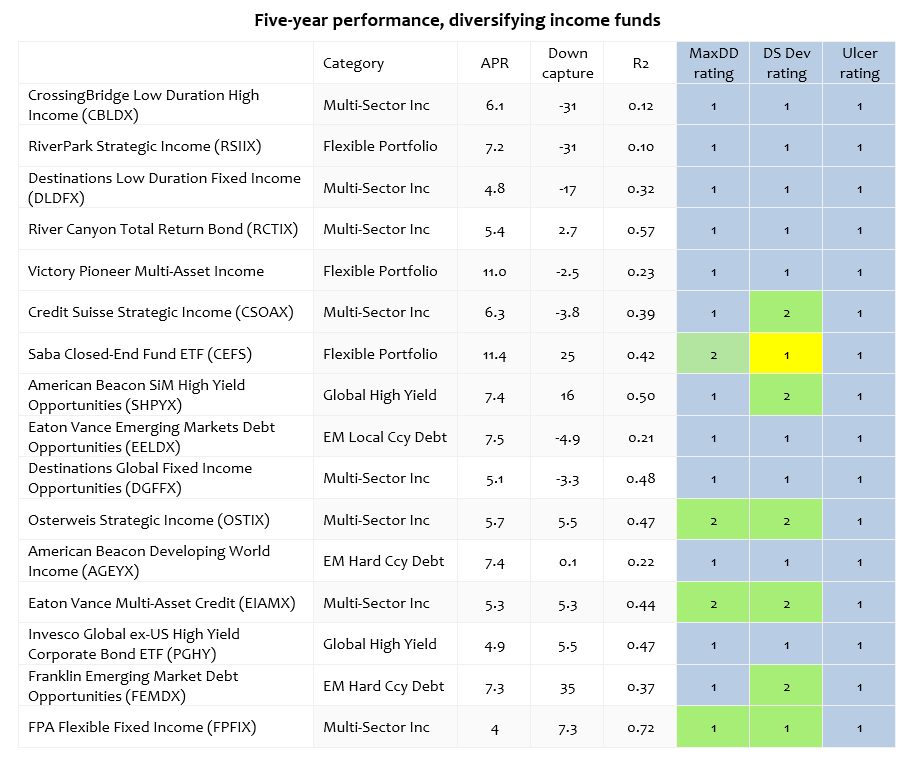

Sixteen funds survived the minimize. The funds are sorted by Sharpe ratio.

learn that chart: The primary three columns are simple. Title, Lipper fund class, and common yearly return over the previous 4 years. Down seize is the share of the US bond market’s draw back that the fund captured. A detrimental down seize means the fund tended to rise when the US bond market fell. The R-squared (R2) measures the diploma of correlation between the fund and the US bond market: 100 implies that the fund marches in lockstep with the bond market; 0 means the fund is totally unbiased of it. Lastly, visible represents of three efficiency metrics: a most drawdown ranking (how far the fund fell relative to its friends), draw back deviation ranking (referred to as “unhealthy deviation,” it’s a measure of how a lot a fund routinely falls relative to its friends) and Ulcer ranking (our favourite: a measure of how far a fund falls and the way lengthy it takes to get better; deep fall + lengthy restoration = huge investor ulcers). In every case, a blue cell alerts high 20% efficiency.

Snapshots of the profitable funds

- CrossingBridge Low Length Excessive Earnings targets excessive present revenue and average capital appreciation by investing in short-maturity excessive yield debt, typically with maturity beneath three years, emphasizing principal safety and decreasing credit score and rate of interest dangers. The fund stands out for its energetic administration within the short-duration phase and prioritizes danger mitigation over chasing yield, aiming for constant revenue with decrease volatility than typical excessive yield funds.

- RiverPark Strategic Earnings pursues revenue and preservation of capital via a versatile, bottom-up portfolio of investment-grade and high-yield company debt, preferreds, convertibles, financial institution loans, and income-producing equities, with common period from 2.5-4 years. Its opportunistic method permits shifting between higher-yielding and extra defensive property as market circumstances dictate, and it’s famous for its skill to put money into particular conditions for potential extra yield in periods of market stress. Nota bene: 4 of the 16 funds on this record rely, a minimum of partially, on the abilities of the CrossingBridge/Cohanzik administration crew. It’s in Snowball’s private portfolio.

- Locations Low Length Fastened Earnings employs a multi-manager technique, which at the moment consists of CrossingBridge Advisors for event-driven excessive yield credit score alternatives and DoubleLine Capital for low period methods. It’s targeted on producing present revenue with low period.

- River Canyon Complete Return Bond employs a bottom-up credit score choice course of with a top-down overlay and goals to establish securities that exhibit upside optionality with draw back safety, specializing in choosing securities with a chance of outperformance throughout a variety of macroeconomic and market situations. It focuses on publicity to securities and sectors which have traditionally low correlation to conventional asset lessons.

- Victory Pioneer Multi-Asset Earnings is a versatile, globally diversified fund investing throughout a large spectrum of income-producing property, together with bonds, dividend-paying equities, and money equivalents. Its strategic asset allocation balances revenue era and long-term progress, making it appropriate for average danger tolerance and dynamic market circumstances. The managers are searching for to use low correlations of worldwide mounted revenue and non-investment grade debt markets with US funding grade markets.

- Credit score Suisse Strategic Earnings combines leveraged loans and high-yield company bonds in a distinguished high-yield technique with the managers adjusting its portfolio’s publicity amongst numerous kinds of debt devices primarily based on market circumstances and outlook, at the moment primarily investing in bonds issued by home and international firms, senior secured floating charge loans, and mortgage-backed securities, asset-backed securities, and CLOs.

- Saba Closed-Finish Fund ETF invests in closed-end funds buying and selling at important reductions to their web asset worth, searching for to generate month-to-month revenue and capital appreciation. The fund distinguishes itself with an activist method, aiming to slim these reductions and unlock worth, and makes use of hedging to mitigate rate of interest danger; its diversified holdings present publicity to each fairness and glued revenue closed-end funds.

- American Beacon SiM Excessive Yield Alternatives gives a versatile method and a willingness to put money into edgier segments of the excessive yield market, which ends up in intervals of elevated volatility in trade for greater potential payouts.

- Eaton Vance Rising Markets Debt Alternatives is a versatile rising markets bond fund that invests throughout sovereign and company credit, native currencies, and off-benchmark alternatives in over 100 nations. Eaton Vance applies rigorous financial and political analysis to construct a portfolio that captures numerous sources of rising market debt revenue, usually shifting past typical benchmarks for enhanced risk-adjusted returns and country-level diversification.

- Locations International Fastened Earnings Alternatives makes use of a multi-manager, multi-sector method to put money into international investment-grade and high-yield bonds, sovereign debt, financial institution loans, most popular securities, and convertibles. The subs embody DoubleLine, Numeric, Man Group, and Cohanzick.

- Osterweis Strategic Earnings pursues long-term capital preservation and average revenue by actively allocating throughout high-yield and investment-grade bonds, with frequent tactical shifts in response to market circumstances. The fund is distinguished by an unconstrained, versatile method from an skilled and lean administration crew, leading to a powerful historic file for risk-adjusted returns, albeit at a manageable volatility stage.

- American Beacon Creating World Earnings pursues revenue via a globally diversified in sovereign and company bonds from rising and frontier markets. It stands out for utilizing 16 managers and several other sub-advisers (International Evolution A/S, abrdn, Sydbank…) specializing in lesser-known nation and sector exposures.

- Eaton Vance Multi-Asset Credit score invests throughout a broad spectrum of credit-related property resembling high-yield bonds, senior loans, structured credit score, most popular and convertible securities, and rising market debt. The fund’s core attraction lies in tactical allocation and an energetic deal with diminished draw back and avoidance of everlasting capital impairment.

- Invesco International ex-US Excessive Yield Company Bond ETF tracks an index of US dollar-denominated, high-yield bonds issued by firms outdoors america. Its distinguishing options embody broad international diversification with a month-to-month rebalance.

- Franklin Rising Market Debt Alternatives invests predominantly in debt obligations from sovereign and sub-sovereign issuers in rising nations, with a versatile method that features choose company debt.

- FPA Versatile Fastened Earnings pursues optimistic absolute returns over any three-year interval – it’s an FPA hallmark – and powerful risk-adjusted returns by investing throughout the mounted revenue universe, unconstrained by benchmark or sector, with a powerful emphasis on capital preservation. Distinctive for its willingness to carry money and cut back danger when alternatives are restricted, FPFIX is run by a seasoned crew at First Pacific Advisors.

Backside line

MFO doesn’t make “promote now!” or “purchase now!” calls, a lot much less predictions about “the ten funds you completely should personal!” These calls are simple to make, inconceivable to make reliably. Our argument is easier: we’re within the midst of a fiscal mess, which is more likely to get messier and messier. It will be prudent, earlier than any panic units in, to look at the query: are there methods to scale back my publicity to rising dangers and nonetheless earn an honest return?

The funds above have made cash over the previous 5 years; the US bond market has not. These funds uniformly goal to supply excessive present revenue with admirably low publicity to the normal revenue markets. And it reminds us, once more, of the constant independence and excellence of the CrossingBridge of us who’re accountable for the 2 highest-rated funds on the record (CrossingBridge Low Length and RiverPark Strategic Earnings).

We are going to attempt to profile three of those funds every month over the past three months of 2025.