{kind=link}

HCL Applied sciences Ltd – Supercharging Progress

HCL Applied sciences Ltd. is a worldwide know-how firm delivering industry-leading capabilities centered round digital, engineering, cloud and AI, powered by a broad portfolio of know-how companies and merchandise. Integrated in 1991 and headquartered in Noida, the corporate at present has a headcount of roughly 219,000 workers throughout 60 nations. HCL caters to purchasers throughout main verticals, offering {industry} options for Monetary Providers, Manufacturing, Life Sciences and Healthcare, Expertise and Providers, Telecom and Media, Retails and Client Packaged Items (CPG) and Public Providers.

Merchandise and Providers

- Engineering and R&D Providers (ERS): Industries reminiscent of ISVs, client electronics, semiconductor, telecom, medical, infrastructure, transportation.

- IT and Enterprise Providers (ITBS): Functions, AI, infrastructure, cloud, digital course of operations.

- Digital Basis Providers: Hybrid and multi-cloud companies, Digital office, networks, cybersecurity, Unified service administration, clever operations.

- Digital Course of Operations: Excessive-speed, agile, environment friendly working fashions, Enterprise transformation options.

Subsidiaries: As of FY24, the corporate has 130 subsidiaries and 6 affiliate corporations.

Development Methods

- AI and GenAI Capabilities: Implementing GenAI options for a significant gaming firm, a European monetary companies agency, a US-based insurance coverage supplier, and a European telecom OEM.

- World Supply Facilities and AI Labs: Opened a brand new supply heart in Patna for IT and engineering companies. Inaugurated an AI Lab in New Jersey and a Generative AI-focused Knowledge Heart in Austin, TX.

- Acquisitions and Sector Growth: Acquired ASAP Group, a German automotive engineering companies supplier, to boost car growth capabilities.

- AI Platforms: Launched HCLTech AI Power and HCLTech Enterprise AI Boundary to spice up enterprise AI initiatives.

Monetary Efficiency

Q1FY25

- Income: Rs. 28,057 crore, up 7% from Rs. 26,296 crore in Q1FY24.

- EBITDA: Rs. 5,793 crore, up 8% from Rs. 5,365 crore in Q1FY24.

- Web revenue: Rs. 4,259 crore, up 21% from Rs. 3,531 crore in Q1FY24.

- Attrition fee: 12.8%, down from 16.3% in Q1FY24.

FY24

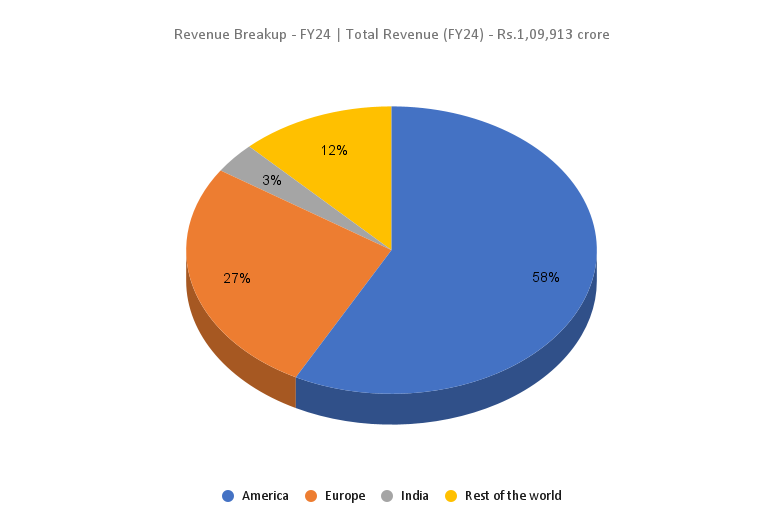

- Income: Rs. 1,09,913 crore, up 8% from FY23, pushed by Service & Software program enterprise momentum.

- Working revenue: Rs. 24,198 crore, up 7% YoY.

- Web Revenue: Rs. 15,702 crore, up 6% YoY.

- Prime-performing verticals: Monetary Providers (12% development), Manufacturing (9.8%), and CPG (8.2%).

Monetary Efficiency (FY21-24)

- Income and PAT CAGR (FY21-24): 13% and 12%, respectively

- Common 3-Yr ROE & ROCE (FY21-24): ~23% and ~28%

- Capital Construction: Debt-to-equity ratio of 0.08.

Trade outlook

- Key Development Driver: The IT & BPM sector is a significant catalyst for the Indian financial system, considerably contributing to GDP and public welfare.

- Digital Adoption: Fast adoption of applied sciences like AI, Cybersecurity, and IoT is enhancing India’s digital capabilities.

- Income Development: The sector is projected to hit US$ 350 billion by 2026 and contribute 10% to India’s GDP.

- Future Projections: India’s know-how {industry} income is predicted to double to US$ 500 billion by 2030.

- Rising Alternatives: Rising applied sciences provide new development alternatives for main IT corporations in India.

Development Drivers

- IndiaAI Mission: Allocation of over ₹10,300 crore (US$ 1.2 billion) permitted to boost India’s AI ecosystem.

- PLI Scheme – 2.0: Budgetary outlay of ₹17,000 crore (US$ 2.06 billion) permitted for IT {Hardware}.

- FDI Rules: As much as 100% FDI permitted in information processing, software program growth, laptop consultancy, software program provide, enterprise and administration consultancy, market analysis, and technical testing companies underneath the automated route.

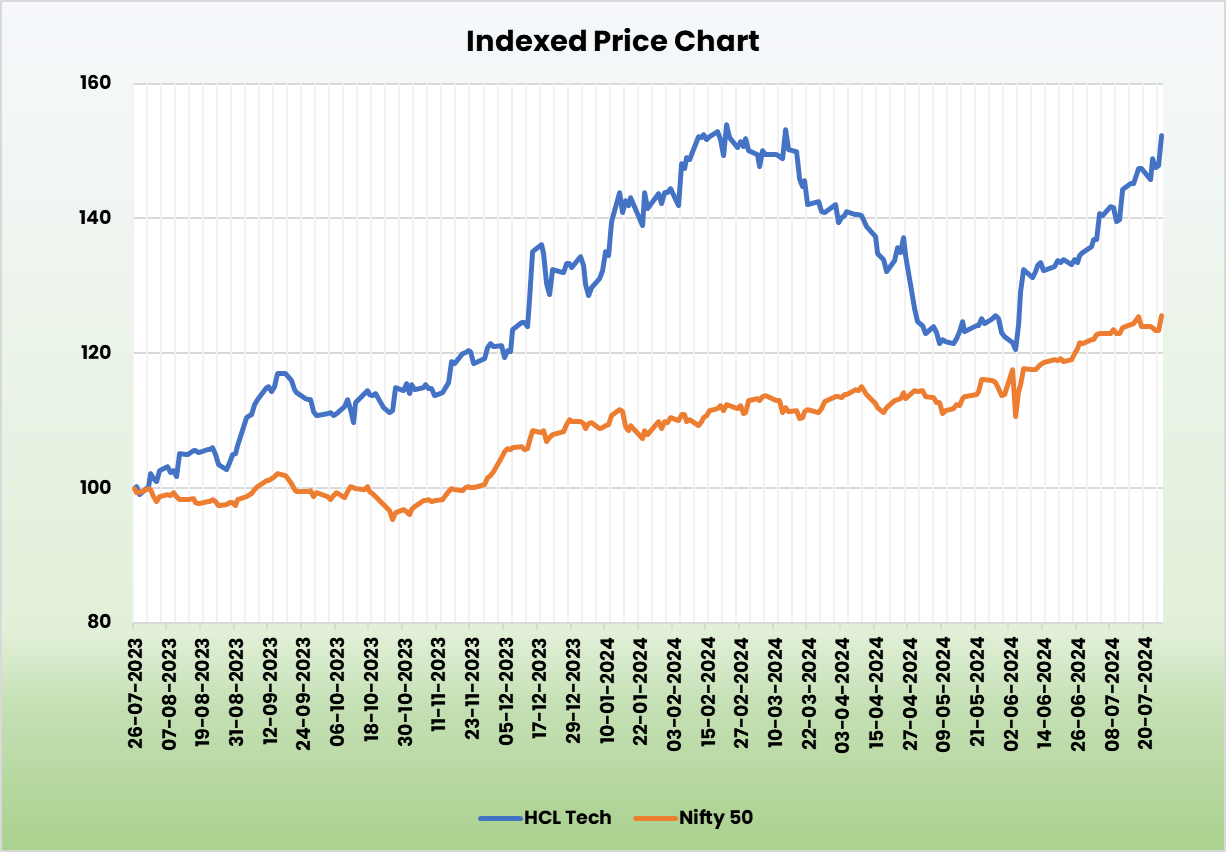

Aggressive Benefit

In comparison with opponents like Wipro Ltd, LTIMindtree Ltd and so on.

HCLTech is buying and selling at an affordable worth with total wholesome efficiency metrics. Notably, the corporate is producing higher revenue margins than its friends.

Outlook

- TCV: Roughly $2 billion in Q1FY25.

- New Offers: Signed 73 massive offers in FY24.

- GenAI: Anticipated to boost income streams.

- Development Expectations: Broad sequential development anticipated throughout all verticals in Q3, besides Monetary Providers.

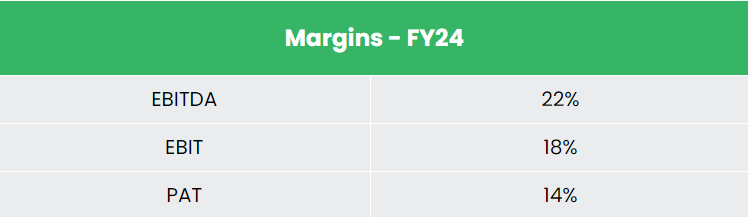

- FY25 Steerage: Income development of three%-5% and EBIT margin of 18%-19%.

Valuation

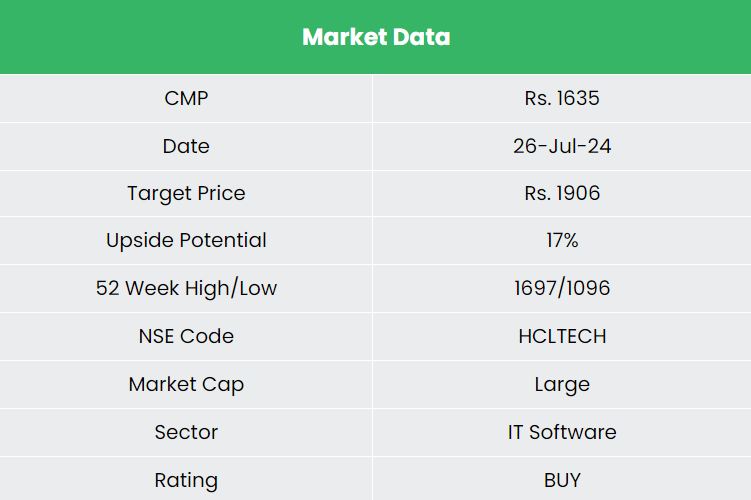

HCL Applied sciences Ltd. is predicted to proceed its development momentum backed by its various order wins and execution capabilities. We advocate a BUY score within the inventory with the goal worth (TP) of Rs. 1,906, 25x FY26E EPS.

Dangers

- Foreign exchange Danger: Important publicity to overseas markets makes the corporate weak to adversarial foreign exchange actions.

- Unsure Demand Setting: Menace of recession in main economies may weaken world circumstances and impression firm development.

Be aware: Please notice that this isn’t a advice and is meant just for instructional functions. So, kindly seek the advice of your monetary advisor earlier than investing.

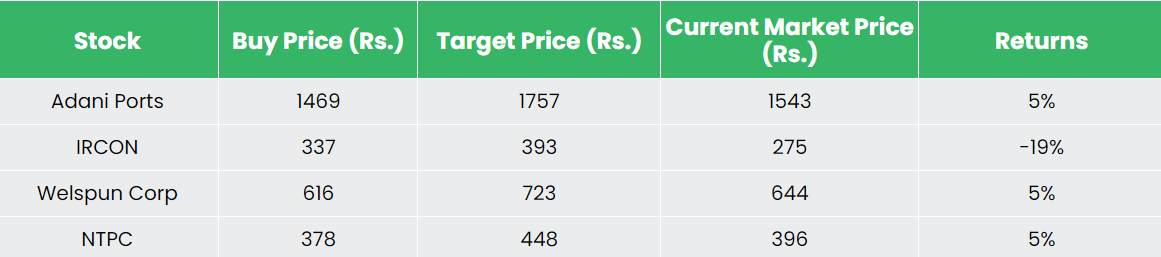

Recap of our earlier suggestions (As on 26 July 2024)

Adani Ports & Particular Financial Zone Ltd

Different articles you could like

Put up Views:

2,703