{kind=link}

A reader asks:

I’m a Marine Corps Infantry Veteran and my spouse is now an Air Power Officer (struck gold). We acquired married and purchased a house in 2020 benefiting from the low charges at 2.4% and have been fortunate sufficient that the house appreciated 25% in 3 years once we have been pressured to promote on account of navy orders altering. By then charges have been means up and we are actually locked into, what I feel, is an overheated market at 6.25%. We’ve got orders arising once more and we’re battling flipping forwards and backwards between shopping for and promoting properties, renting the house we personal out, or simply calling it quits and promoting and renting ourselves till she is out of the navy. Any recommendation on pressured timing?

We get a whole lot of attention-grabbing questions on Ask the Compound from members of the armed companies. I’m certain this can be a matter many service members have grappled with.

Homeownership was already the American Dream however the 2020s took the FOMO to new ranges for individuals who missed out on the best housing bull market this nation has ever seen.1

In the event you didn’t personal a house it nearly felt irresponsible regardless that nobody might have presumably predicted a pandemic would trigger the most important dwelling value enhance on file.

Right here’s the factor — proudly owning a house is just not for everybody. That is true whatever the course of dwelling costs.

There are a lot of advantages to homeownership. A home is a good inflation hedge. It’s a spot to name your individual, so there may be psychic earnings concerned. You’ll be able to construct fairness over time so it’s a good financial savings automobile.

However there are downsides to homeownership.

A home is an illiquid monetary asset. You’ll be able to’t spend it. It’s almost inconceivable to calculate the return on funding. There are a great deal of ancillary prices connected to a house. The frictions concerned make it pricey to purchase and promote. You lose flexibility when proudly owning a house.

These final two factors are a very powerful variables for this query.

When shopping for a house there are closing prices and shifting prices. Then while you promote you pay these once more along with realtor charges.

You additionally should keep in mind the truth that the vast majority of your funds early within the lifetime of a mortgage go in the direction of servicing the debt.

That wasn’t nice when charges have been 2.4%. Within the first few years of a 30 12 months mounted price mortgage you’d be paying roughly half of your month-to-month fee to principal and half to curiosity.

However issues are a lot worse at increased mortgage charges.

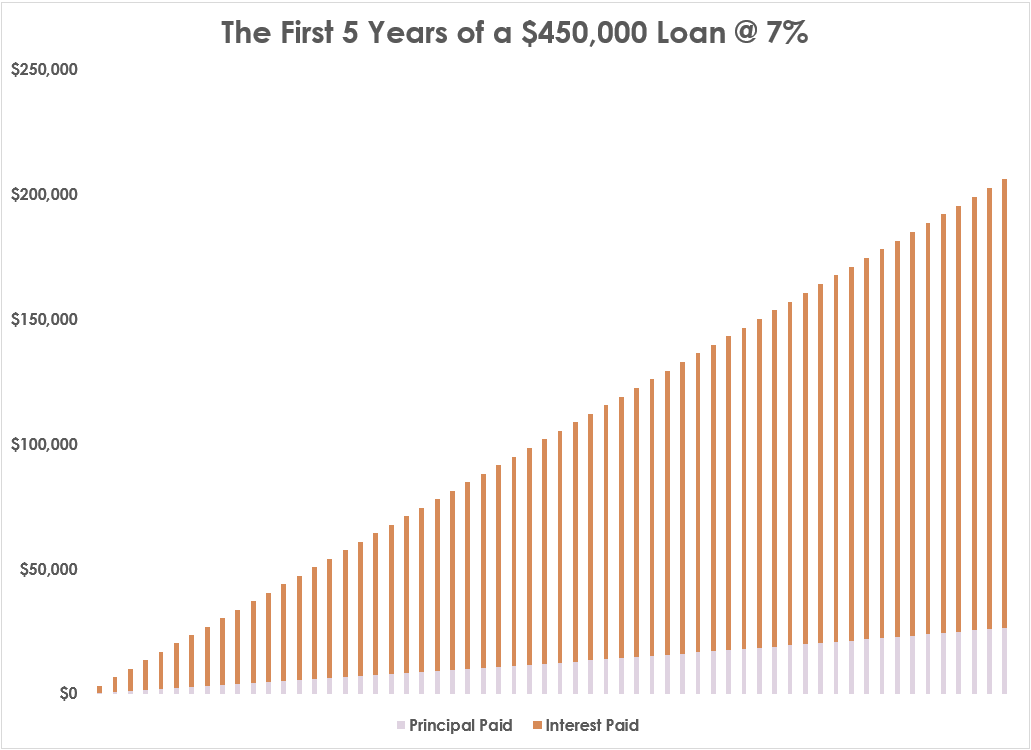

Right here’s a take a look at the breakdown between principal and curiosity funds within the first 5 years of a 30 12 months mounted price mortgage of $450k at prevailing charges of seven%:

Simply 12% of the month-to-month fee goes in the direction of principal reimbursement on the outset. Even after 60 funds you’d nonetheless see 17% go to principal whereas 83% of the month-to-month fee goes to curiosity.

On a 7% mortgage the principal paydown doesn’t match the curiosity a part of the fee till 12 months 20. Clearly, the hope could be you would refinance sooner or later.

However the principle takeaway right here is that purchasing a house and proudly owning it for just a few years is a really excessive hurdle price after factoring in all charges, bills and the character of the funds early within the lifetime of the mortgage.

You would want to expertise some wholesome value positive factors to make the maths work. Now, you would additionally take an interest-only mortgage however now’s merely not a good time to be in the home buying and selling enterprise.

Think about the truth that demand has slowed to a crawl as a result of consumers don’t wish to tackle 7% mortgage charges and you would be caught proudly owning a house you don’t need anymore while you get deployed to a different base.

There are many private finance specialists who look down on renting.

Why would you pay another person’s mortgage for them???

I’m a home-owner but it surely’s not for everybody.

The funds actually matter in a call like this however you even have to consider the headache ratio on these selections.

Renting provides you far more flexibility and permits you to keep away from the numerous stresses that exist within the home-buying and promoting course of.

It’s arduous to place a value on flexibility particularly when your way of life requires it.

Homeownership isn’t for everybody.

We coated this query on the final Ask the Compound of 2024:

We additionally hit on questions in regards to the optimum financial savings price for retirement, coated name choice methods vs. bonds, how you can hedge your actual property portfolio and a few funding recommendation for an 18 12 months previous investor who needs to retire a multi-millionaire.

Additional Studying:

What’s the Historic Charge of Return on Housing?

1I suppose you would discuss me into the land seize within the 1800s like Tom Cruise in Far & Away.

This content material, which accommodates security-related opinions and/or info, is offered for informational functions solely and shouldn’t be relied upon in any method as skilled recommendation, or an endorsement of any practices, services or products. There might be no ensures or assurances that the views expressed right here might be relevant for any specific info or circumstances, and shouldn’t be relied upon in any method. It’s best to seek the advice of your individual advisers as to authorized, enterprise, tax, and different associated issues regarding any funding.

The commentary on this “submit” (together with any associated weblog, podcasts, movies, and social media) displays the non-public opinions, viewpoints, and analyses of the Ritholtz Wealth Administration workers offering such feedback, and shouldn’t be regarded the views of Ritholtz Wealth Administration LLC. or its respective associates or as an outline of advisory companies offered by Ritholtz Wealth Administration or efficiency returns of any Ritholtz Wealth Administration Investments shopper.

References to any securities or digital property, or efficiency knowledge, are for illustrative functions solely and don’t represent an funding advice or supply to supply funding advisory companies. Charts and graphs offered inside are for informational functions solely and shouldn’t be relied upon when making any funding resolution. Previous efficiency is just not indicative of future outcomes. The content material speaks solely as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these supplies are topic to alter with out discover and should differ or be opposite to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Administration, receives fee from varied entities for ads in affiliated podcasts, blogs and emails. Inclusion of such ads doesn’t represent or indicate endorsement, sponsorship or advice thereof, or any affiliation therewith, by the Content material Creator or by Ritholtz Wealth Administration or any of its workers. Investments in securities contain the chance of loss. For added commercial disclaimers see right here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures right here.