")

{kind=link}

EIH Ltd – Leaders in luxurious hospitality

Established in 1949, EIH Ltd. is likely one of the largest luxurious resort chains in India. A flagship firm of The Oberoi Group, the corporate owns and operates 30 lodges, resorts, and luxurious cruisers throughout 7 international locations and 22 cities underneath the model names Oberoi, Trident and Maiden. Along with personal properties, the corporate can also be following an asset mild mannequin by signing operations and administration contracts with third events. As of FY24, the corporate owns a portfolio of 4,269 keys (owned and managed) throughout all classes. The corporate’s companies additionally embrace flight catering, airport lounge, journey planning, company air charters and so on.

Merchandise and Companies

The corporate’s enterprise actions comprise of:

- Lodge companies – Lodging, meals & beverage and different companies offered by resort, inns, resorts, vacation properties, eating places, caterers, and so on.

- Actual Property Actions – Renting of funding properties.

Subsidiaries: As of FY24, the corporate has 9 subsidiaries, 3 affiliate firms and three joint ventures.

Funding Rationale

- Enlargement plans – EIH plans to open 20 new properties, totalling 1,350 keys, by 2029. The portfolio will embrace a mixture of lodges, boats, and cruises throughout each home and worldwide markets, both owned outright or developed via joint ventures and partnerships. The growth additionally includes the creation of mixed-use developments with industrial, retail, and F&B areas. Within the home market, three lodges are set to open in 2025 and 2026. Internationally, the corporate goals to launch two lodges, two luxurious boats, and a cruiser throughout the identical timeframe. Notably, EIH is getting into the London market with a luxurious resort in Mayfair, exploring partnership alternatives to scale back its publicity. This 21-key resort is slated to open in 2028. These growth efforts are anticipated to drive profitability, strengthen the model, and assist a various and sustainable enterprise mannequin for the corporate.

- Sturdy operational efficiency – The corporate noticed notable development in RevPAR (Income per Out there Room) throughout all its enterprise segments. In Q2FY25, in comparison with the identical interval final yr, Oberoi Metro noticed a ten% enhance, Oberoi Leisure improved by 7%, and each Trident Metro and Trident Leisure rose by 22% every. Occupancy charges grew from 69% to 72%, whereas the Common Room Charge (ARR) rose to Rs.14,973 within the final quarter, in comparison with the Rs.13,732 throughout the identical interval within the earlier yr. Total, these efficiency positive factors replicate the corporate’s operational success, market power, and monetary stability, setting the stage for continued development and profitability.

- Q2FY25 – EIH reported its highest ever quarterly income and revenue through the interval. The corporate generated income of Rs.589 crore marking a rise of 11% in comparison with the Rs.531 crore income of Q2FY24. EBITDA stood at Rs.208 crore in opposition to the Rs.165 crore of Q2FY24, a development of 26% YoY. Web revenue stood at Rs.133 crore which is a development of 41% as in comparison with the Rs.94 crore of the identical interval within the earlier yr. The corporate is money optimistic with ~Rs.711 crore.

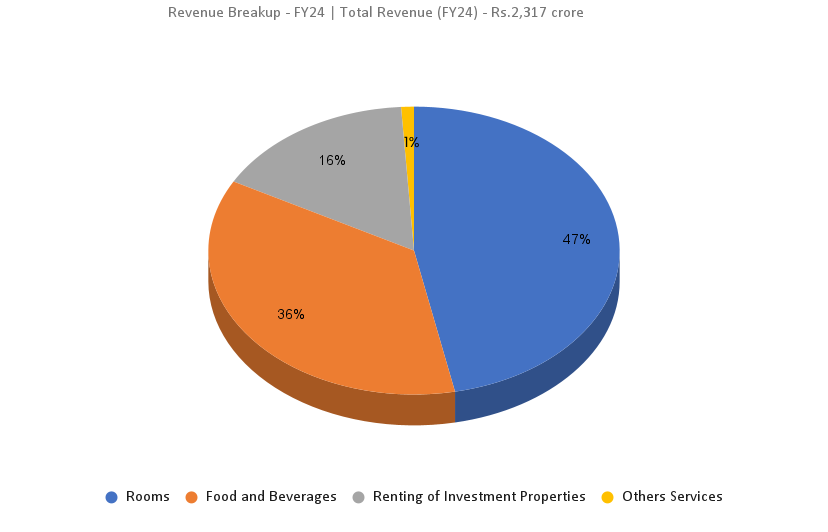

- FY24 – The corporate generated income of Rs.2,317 crore, a rise of 26% in comparison with FY23 income. Working revenue is at Rs.911 crore, up by 46% YoY. The corporate posted a web revenue of Rs.521 crore, a rise of 63% YoY. FY24 working revenue margin is at 39% and web revenue margin is at 22%.

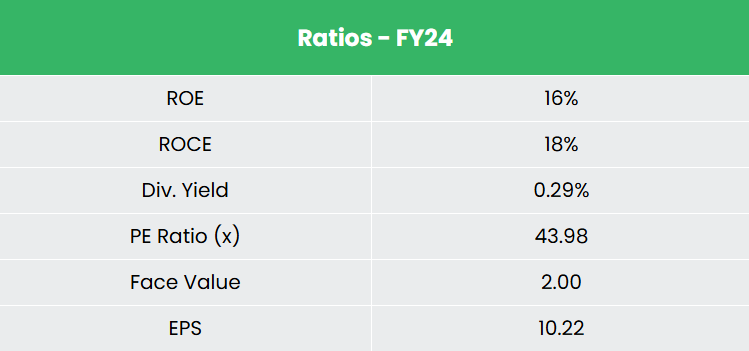

- Monetary Efficiency – EIH has generated income and web revenue CAGR of 72% and 56% over the interval of three years (FY21-24). The typical 3-year ROE & ROCE is round 9% and 12% for the FY21-24 interval. The corporate has a robust steadiness sheet with a strong debt-to-equity ratio of 0.05.

Business

Tourism and Hospitality is one the most important service industries in India, enjoying an important position in driving the nation’s development and prosperity. With its various geography and wealthy cultural heritage, India presents a variety of distinctive experiences, positioning it as one of many prime locations for worldwide tourism spending. By 2028, the sector is projected to generate over US$ 59 billion in income, with International Vacationer Arrivals (FTAs) anticipated to achieve 30.5 million. In accordance with the World Journey and Tourism Council (WTTC), India’s Journey & Tourism GDP is anticipated to develop at a median price of seven.1% yearly over the following decade. The nation is eyeing for additional growth within the sector via initiatives comparable to wellness tourism, culinary tourism, and eco-tourism.

Development Drivers

- Authorities initiatives like Swadesh Darshan 2.0, e-visa amenities, RCS-UDAN Scheme that had been launched to energy the sustainable imperatives within the tourism sector.

- 100% International Direct Funding (FDI) allowed within the tourism business underneath automated route.

- Within the Interim Finances 2024, Rs.2,449.62 crore (US$ 294.8 million) was allotted to the tourism sector.

Peer Evaluation

Rivals: Chalet Motels Ltd, Lemon Tree Motels Ltd, and so on.

In comparison with the above opponents, EIH is essentially the most undervalued inventory with sturdy returns on the capital invested and wholesome development in gross sales.

Outlook

The corporate’s growth technique, which incorporates 20 properties throughout key world and home markets, exhibits robust potential. These efforts are anticipated to drive income development, broaden geographic attain, and diversify the corporate’s market presence. The corporate plans to increase its portfolio of mixed-use growth initiatives, incorporating each residential and industrial areas, which is anticipated to spice up returns and profitability. It anticipates improved income and profitability within the second half of FY25. Moreover, the corporate goals so as to add roughly 216 keys in 2025 and 2026.

Valuation

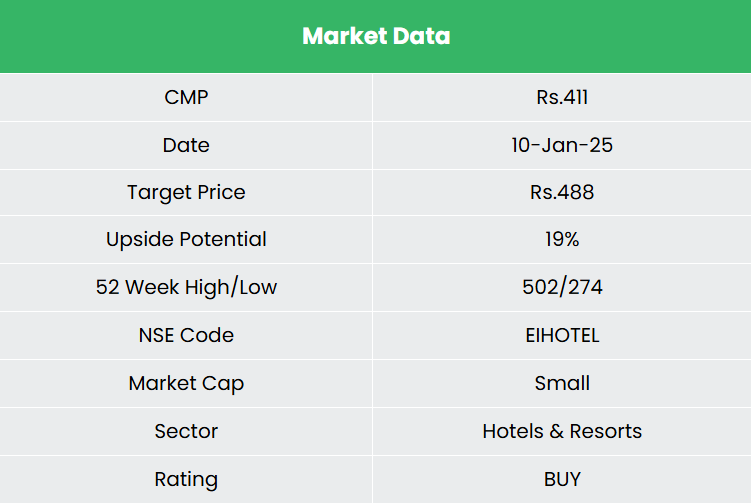

The corporate’s steady operational efficiency and upcoming growth plans are anticipated to maintain its development momentum. We advocate a BUY ranking within the inventory with the goal value (TP) of Rs.488, 39x FY26E EPS.

Threat

- Macroeconomic components – Any financial slowdown within the nation might influence the demand for the journey business thereby impacting the corporate turnover.

- Launch of latest lodges – Any delay within the launch of latest lodges/cruises will influence profitability.

Word: Please be aware that this isn’t a advice and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

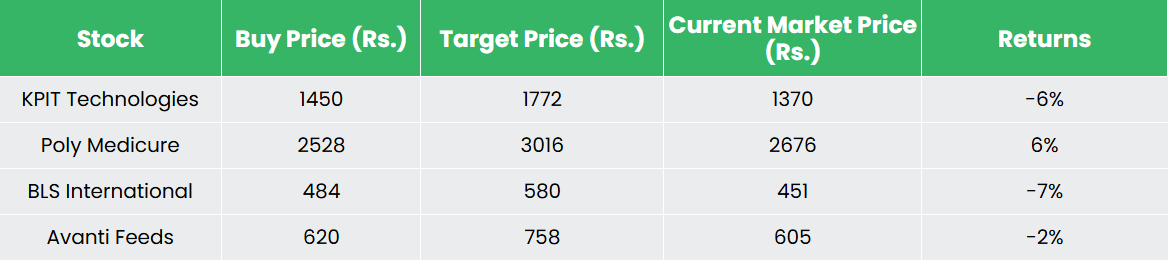

Recap of our earlier suggestions (As on 10 January 2024)

Different articles chances are you’ll like

Put up Views:

596