{kind=link}

Basically, I prefer to play contrarian as a result of it’s good to contemplate different viewpoints.

As an alternative of merely regurgitating the identical take, typically going towards the grain can repay.

Actually, the consensus usually will get it incorrect, whether or not it’s the trajectory of house costs or the path of mortgage charges.

The newest anticipated headwind for mortgage charges dropped late Friday when Moody’s downgraded the US’ credit standing.

But when we zoom out a tad, this might finish of serving to mortgage charges. Permit me to clarify.

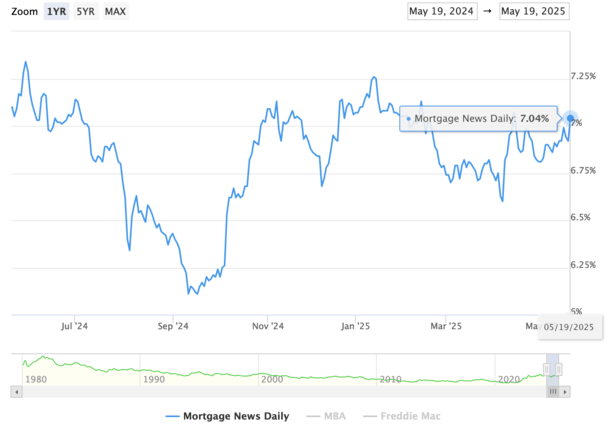

Preliminary Response Isn’t Nice, Mortgage Charges Again Above 7%

The 30-year fastened is again above 7%, once more (once more!), per the newest every day studying from Mortgage Information Each day.

It has been seesawing round these ranges for some time now, and it’s yet one more intestine punch for potential house patrons.

Once more, no enormous distinction between a charge of 6.875% and seven% by way of month-to-month cost, however the psychology might be brutal.

Seeing a 7 as a substitute of a 6 whereas additionally presumably being stretched to start with isn’t good for debtors or the broader housing market.

As such, mortgage functions would possibly face much more of an uphill battle because the spring house shopping for market begins to fizzle.

I also needs to observe that the 30-year fastened is now solely 5 bps beneath its year-ago ranges. So decrease mortgage charges are now not a function of the 2025 spring house shopping for season.

Mortgage Fee Spreads Received Worse on the Downgrade Information

What’s attention-grabbing is the 10-year bond yields that dictate mortgage charges barely elevated for the reason that Moody’s information was introduced.

Yields on the bellwether bond had been up lower than 5 foundation factors (bps) at present, which might point out comparatively flat mortgage charges.

As an alternative, the 30-year fastened was up a large 12 bps to 7.04%, per MND. In different phrases, mortgage spreads widened pretty aggressively on the information.

The unfold between the 30-year fastened and the 10-year bond yield has traditionally been round 170 bps.

That is the premium traders demand for taking a threat on a borrower’s house mortgage versus a assured authorities bond.

In recent times this unfold widened because the Fed stopped shopping for mortgages and volatility elevated.

Spreads obtained actually vast (over 300 bps) earlier than coming all the way down to the decrease 200 vary, however jumped again above 250 bps once more.

So traders are demanding extra premium above Treasuries to purchase mortgage-backed securities (MBS), although this might reasonable as time goes on.

However the truth that it was largely spreads, and fewer so yields rising, is a optimistic signal relating to the credit score downgrade, a minimum of in my thoughts.

What Does Moody’s Downgrade Imply for Mortgage Charges?

As you may see, the early response wasn’t optimistic for mortgage charges, however as I identified, it’s largely worsened spreads.

After the mud settled, 10-year Treasuries have come down fairly a bit, reaching 4.56% earlier than settling round 4.49%.

It arguably helped that Moody’s introduced the US downgrade late on Friday.

That gave the market time to digest the information with out having to make any kneejerk reactions.

Had they introduced the transfer within the morning, or midweek, likelihood is markets would have been fairly rattled.

As an alternative, merchants (and the media) got a pair days to make sense of all of it and draw their very own conclusions.

And eventually look the inventory market was holding up fairly nicely, with the Dow up on the day and the S&P 500 about flat.

That’s fairly good contemplating all of the doom and gloom that was swirling a pair days in the past when the information was introduced.

In the end, Moody’s merely matched different score businesses who had already minimize the U.S. score years in the past.

Customary & Poor’s downgraded the U.S. score from its high tier AAA to AA+ all the best way again in August 2011.

And Fitch Rankings did the identical in August 2023. So Moody’s was merely catching up with the others.

As for why, Moody’s mentioned “massive fiscal deficits will drive the federal government’s debt and curiosity burden greater.”

Briefly, an excessive amount of authorities spending, an excessive amount of debt, and rising curiosity funds on mentioned debt.

However right here’s why that would wind up being a superb factor for mortgage charges. The rankings company is mainly telling the federal government to get its act collectively.

They held out so long as they might, however lastly downgraded the U.S., maybe as a warning to do higher. To make modifications earlier than issues get even worse.

So in my thoughts, whereas everyone seems to be reporting that the 30-year fastened is again above 7%, I’m optimistic that it might power lawmakers to rein it in.

This growth might truly push politicians to make extra concessions on the “huge, lovely invoice” so spending and Treasury issuance doesn’t spiral uncontrolled.

And within the course of, that would truly assist ease bond yields and in flip result in decrease mortgage charges.

Simply observe that it won’t be rapid, so this might current yet one more near-term headwind.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house patrons higher navigate the house mortgage course of. Comply with me on X for warm takes.