{kind=link}

The CPI inflation report launched this week confirmed that it’s going to be tough to shut out the ultimate mile within the struggle in opposition to inflation. Nonetheless, because of that report, it looks as if buyers are lastly coming to grips with the Fed’s message of upper charges for longer.

I really feel snug saying there’ll proceed to be volatility, each up and down, because the markets react to the month-to-month inflation information studies. If the inflation information helps charge cuts, markets will seemingly go up. If the inflation information helps leaving charges alone, markets are prone to go down.

For instance, this Tuesday (2/13) there have been marginally increased CPI inflation readings than what the analysts anticipated. Properly, that despatched the S&P 500 down -1.4% and the Nasdaq down round -1.6% on the day. Largely as a result of the markets interpreted this dataset as a purpose for the Fed NOT to chop rates of interest.

However too many individuals like to oversimplify the impacts from Fed charges by saying, “Excessive charges/charge hikes are unhealthy for shares, and low charges/charge cuts are good for shares.” Positive, the sentiment of that relationship is usually true, however it’s by no means that straightforward.

If that’s all you’re fixated on in relation to the Fed, I feel you might be lacking what’s in all probability most essential to buyers: the flexibility to plan round a major interval with increased rates of interest.

Impacts of Charge Instability & Uncertainty

Rate of interest ranges feed into each a part of the financial system. The speed set by the U.S. Federal Reserve is a key element to establishing rates of interest for numerous loans, curiosity funds and different yield-focused investments. If you wish to try to guess which path charges are headed, begin with the speed set by the U.S. Fed. Wherever it goes—up, down, or sideways—the consequences filter via into the broader financial system.

For the reason that finish of the pandemic, rates of interest have been on the rise. Starting in March 2022, the Fed went from a virtually 0% charge to over 5% in roughly a 12 months. Arguably probably the most painful half was the staggering velocity of those hikes.

It’s robust for a enterprise or a person to successfully plan for his or her long-term future when there’s that a lot volatility in rates of interest and borrowing prices. Uncertainty round charges may cause many buyers and enterprise leaders to delay main purchases or investments till they’ve extra readability.

Frankly, I don’t blame them.

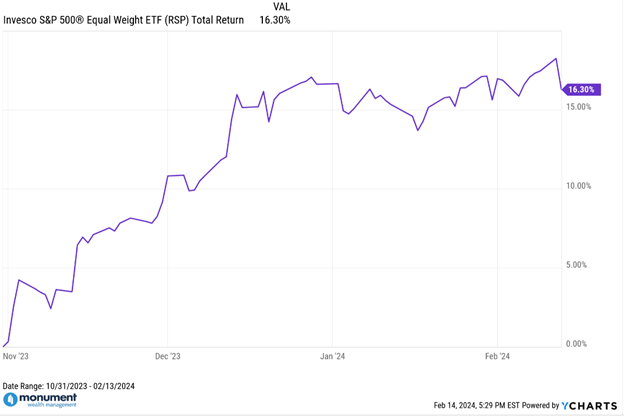

Fortunately, evidently the Fed has signaled an finish to this mountaineering cycle throughout its previous couple of conferences. Eradicating among the unknowns round charges is without doubt one of the major causes we’ve seen broad market rallies just like the equal-weight S&P 500 ETF (ticker: RSP) being up round +16.3% whole return from 10/31/23 via 2/13/24 (see chart beneath).

It’s not a coincidence that there was additionally a Fed assembly on the finish of October. Right here’s an instance of upside volatility attributable to the Fed.

With out the concern of charges shifting considerably increased, it ought to give enterprise leaders the chance to begin planning and financing longer-term investments that may enhance future development. That’s excellent news for buyers on the lookout for the following wave of development. Sure, the price of debt is increased than a number of years in the past, but when charges aren’t prone to rise considerably sooner or later, corporations and buyers can appropriately issue that into the funding choices being made at the moment.

Discovering A New “Regular” for Curiosity Charges

Larger charges develop into much less of a storyline on your portfolio when you’ll be able to plan for them forward of time, however that solely works if charges keep comparatively flat. Fortunately, the Fed’s purpose isn’t to be persistently making main strikes. What they need is for charges to discover a new regular or a “impartial” degree.

The Fed is thought for its twin mandate which boils right down to low unemployment and manageable inflation. By doing that they’re making an attempt to create a “impartial” financial system that’s neither too scorching nor too chilly. An financial system that’s too chilly is rising beneath development or mentioned in another way, is likely to be leaving financial meat on the bone. However an financial system that runs too scorching can result in runaway inflation.

So, what’s the precise “impartial” rate of interest for the Fed?

Whereas it’s unimaginable to know for positive, the Fed itself has estimated it to be round 2.5% when inflation is at its 2% goal, or round 0.50% above the present inflation as defined on this Reuters article. So, with inflation presently round 3%, then “impartial” within the Fed’s eyes is likely to be round 3.5%.

Curiously, I feel it’s additionally very attainable that the “impartial” charge degree post-pandemic has truly moved increased than the beforehand estimated 2.5% like this article written by the Minneapolis Fed President suggests. The next “impartial” charge would imply the Fed wants to chop even much less from right here as inflation strikes again down in the direction of their goal.

With the Fed charges presently sitting at 5.25% to five.50%, they’re doing precisely what they mentioned they’d: Taking a restrictive stance and staying like that till they’re completely snug inflation is effectively below management. It’s going to be a while earlier than the Fed decides to return to a “impartial” charge coverage, and that “impartial” is likely to be even increased than what it was earlier than.

All of because of this rates of interest in all probability gained’t be shifting a complete lot decrease from right here.

0% Curiosity Charges Are Gone: Get Comfy with the New “Regular”

Let’s be trustworthy, all of us bought used to 0% rates of interest and free cash. Companies might simply finance short-term development initiatives with out an excessive amount of concern of future penalties and prices. Cash was so low-cost that many companies and buyers didn’t create and comply with via on a long-term plan.

That’s not the case anymore.

Gone are the times of 0% rates of interest, no less than for the foreseeable future, however that doesn’t imply the world is ending. All it means is that corporations and buyers have to adapt to what may very well be a long-term development of upper charge ranges in the event that they haven’t already. Everybody knew rates of interest had been going to need to go up finally whether or not they admitted it or not. It’s not wholesome, regular, or sustainable for an financial system to completely have 0% charges.

So, if you happen to locked in low charges years in the past, kudos to you. Journey that for so long as you’ll be able to. Nonetheless, if you happen to’ve been delaying a purchase order or funding in hopes of timing a drop in charges, possibly it’s time to rethink. Who is aware of how lengthy you is likely to be ready at this level?

(Additionally, don’t ever attempt to time the monetary markets. EVER.)

Proper now, the mix of the financial information and the Fed’s public messaging of “increased for longer” make it seem to be there are minimal charge cuts on the horizon. Whereas that may make borrowing dearer, planning on your investments ought to be simpler now that there’s doubtlessly extra stability, and possibly even some predictability in charge ranges.