Insights")

{kind=link}

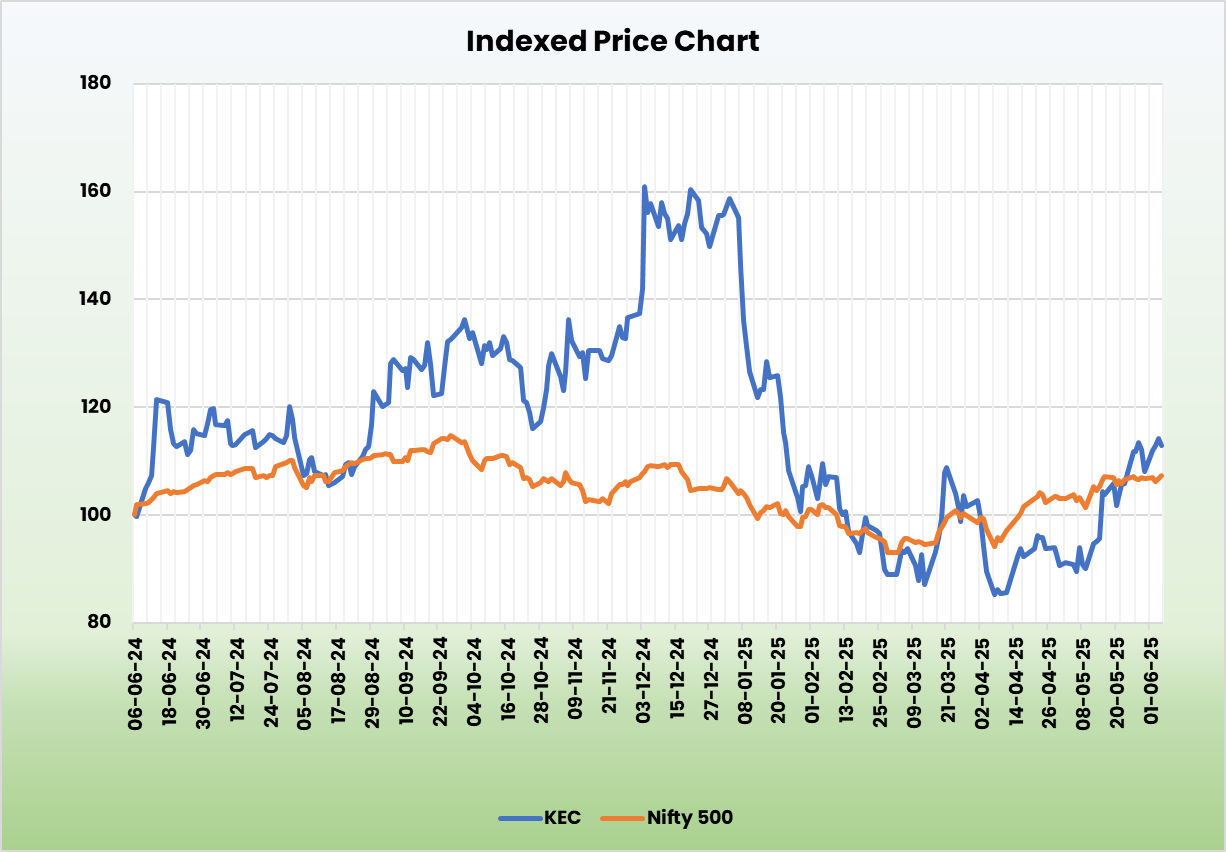

Okay E C Worldwide Ltd – Constructing Sustainable Infrastructure

Integrated in 2005 and headquartered in Mumbai, Okay E C Worldwide Ltd. is a world chief in infrastructure options. The flagship firm of RPG Group, KEC is an Engineering, Procurement, and Building (EPC) main delivering initiatives in key infrastructure sectors equivalent to energy transmission & distribution, civil, transportation, renewables, oil and gasoline pipelines and cables. As of 31 March 2025, the corporate has 8 manufacturing services and 275+ ongoing initiatives in 8 strategic enterprise items unfold throughout 110+ international locations.

Merchandise and Providers

KEC Worldwide is primarily engaged within the following enterprise:

- Infrastructure Initiatives (EPC) – The corporate undertakes Engineering, Procurement, and Building (EPC) initiatives throughout a variety of sectors, together with utilities, railways, buildings, industrial services, and civil infrastructure. Its core focus areas embrace the development, erection, and upkeep of energy transmission strains, railway programs, and different civil engineering works.

- Electrical Gear Manufacturing – KEC additionally manufactures electrical tools, with a key emphasis on the manufacturing of electrical wires and cables.

Subsidiaries: As of FY24, the corporate has 17 subsidiaries and 1 affiliate firm.

Funding Rationale

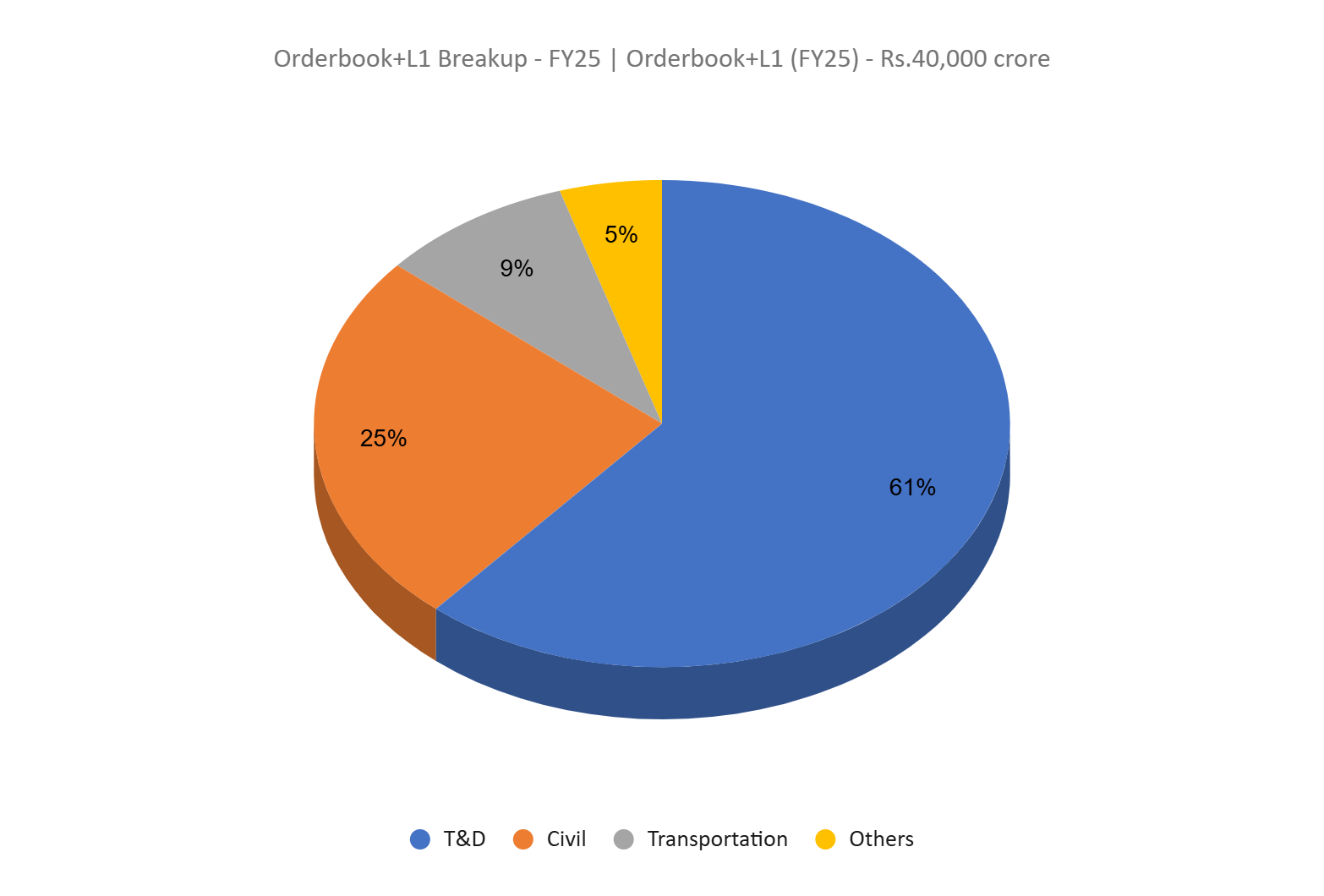

- Increasing order ebook – KEC Worldwide has considerably expanded its order ebook, recording a 36% YoY progress in FY25 with complete orders price Rs.24,689 crore, led primarily by the Transmission & Distribution (T&D) section, which contributed 70% of the consumption. The corporate secured numerous orders throughout geographies, together with key wins in India, the Center East, and the Americas, and marked its entry into new segments equivalent to semiconductors and upstream metal initiatives. Notable achievements embrace its first STATCOM order and elevated common order measurement from Rs.200 crore to Rs.325 crore. The order ebook stood at Rs.33,398 crore on the finish of FY25, with the order ebook plus L1 pipeline exceeding Rs.40,000 crore, offering robust income visibility for the subsequent 6 – 8 quarters. The corporate has gained a number of orders from Energy Grid Company of India Ltd, notably within the excessive margin HVDC (Excessive-Voltage Direct Present) section. FY26 YTD order consumption is at Rs.4,200, a strong 40% YoY progress.

- Segmental efficiency – The corporate is focusing on robust progress in its Transmission & Distribution (T&D) section. The section reported income of Rs.12,833 crore, marking a 23% YoY enhance. Order consumption surged by 60% to Rs.18,000 crore. To leverage rising alternatives, the corporate is increasing tower manufacturing capability at its Dubai, Jaipur, and Jabalpur services. The transportation section additionally gained momentum, recording order inflows of Rs.2,200 crore, together with preliminary orders within the ropeway and gauge conversion sectors. Through the fiscal yr, the corporate efficiently accomplished its first Prepare Collision Avoidance System (TCAS) challenge beneath the Kavach initiative and secured further orders. In the meantime, the cables enterprise achieved its highest-ever income, revenue, and order consumption. The corporate additionally commissioned an aluminium conductor plant and is now working to double its capability. Investments have been made towards an e-beam facility and elastomeric cable manufacturing, each of that are progressing as deliberate.

- Q4FY25 – Through the quarter, the corporate generated income of Rs.6,872 crore, a rise of 11% in comparison with the Rs.6,165 crore of Q4FY24. Working revenue elevated from Rs.388 crore of Q4FY24 to Rs.539 crore of Q4FY25, a progress of 39%. The corporate reported web revenue of Rs.268 crore, a rise by 76% YoY in comparison with Rs.152 crore of the corresponding interval of the earlier yr.

- FY25 – Through the FY, the corporate generated income of Rs.21,847 crore, a rise of 10% in comparison with the FY24 income. Working revenue is at Rs.1,504 crore, up by 24% YoY. The corporate reported web revenue of Rs.571 crore, a rise of 65% YoY.

- Monetary Efficiency – The three-year income and web revenue CAGR stands at 17% every between FY23 – 25. TTM gross sales and web revenue progress is at 10% and 65%. Common 3-year ROE and ROCE is round 9% and 15% for FY23-25 interval. Debt to fairness ratio is at 0.74.

Business

India’s electrical tools market is projected to develop from US$ 52.98 billion in 2022 to US$ 125 billion by 2027, at a powerful CAGR of 11.7%. The engineering sector, which underpins infrastructure and manufacturing, stays a strategic pillar of the Indian economic system, supported by aggressive benefits in price, expertise, and innovation. Energy infrastructure continues to see heavy funding, with over US$ 107 billion earmarked for transmission growth by 2032. The sector is transitioning towards clear vitality and common entry, pushed by coverage assist and rising demand. Concurrently, the development tools market is predicted to develop at 8.3% CAGR by 2030. Bold initiatives like metro expansions and Indian Railways’ modernization additional strengthen long-term business prospects.

Progress Drivers

- With the purpose to just about triple its renewable vitality capability and guarantee 24×7 energy entry nationwide, India plans to speculate over Rs. 9.15 lakh crore (US$ 107 billion) by 2032 to construct further transmission strains.

- The federal government has de-licensed the engineering sector with 100% FDI permitted.

- Authorities has allowed 100% FDI within the railway sector and renewable vitality sector.

Peer Evaluation

Opponents: Kalpataru Initiatives Worldwide Ltd.

In comparison with its rivals, the corporate is producing secure returns from invested capital backed by a constant enhance in gross sales, indicating the administration’s prudent capital allocation methods.

Outlook

The administration has projected a income progress of 15% for FY26, together with an EBITDA margin goal of 8% to eight.5%. Order consumption for FY26 is predicted to be roughly Rs.30,000 crore, with the Transmission & Distribution (T&D) section contributing round 70%. The corporate continues to prioritize increasing capability inside its present product strains, whereas additionally exploring alternatives in area of interest markets. The order pipeline stays strong throughout all key enterprise segments. Going ahead, well timed execution of orders and efficient price optimization shall be essential areas to watch.

Valuation

The federal government’s elevated deal with transmission and distribution (T&D), coupled with rising energy demand and the corporate’s strategic efforts to develop its cables enterprise, positions the corporate as a powerful and dependable funding alternative. We suggest a BUY score within the inventory with the goal worth (TP) of Rs.1,051, 31x FY27E EPS.

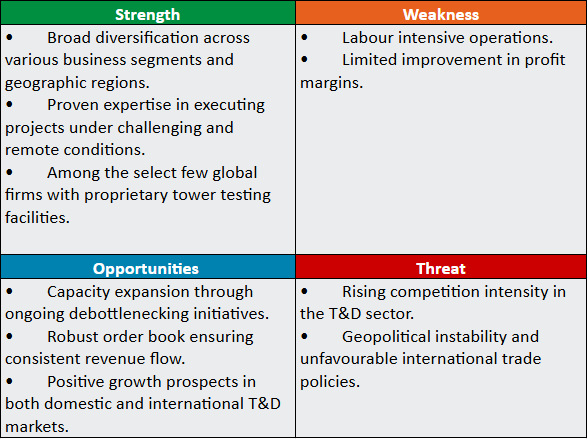

SWOT Evaluation

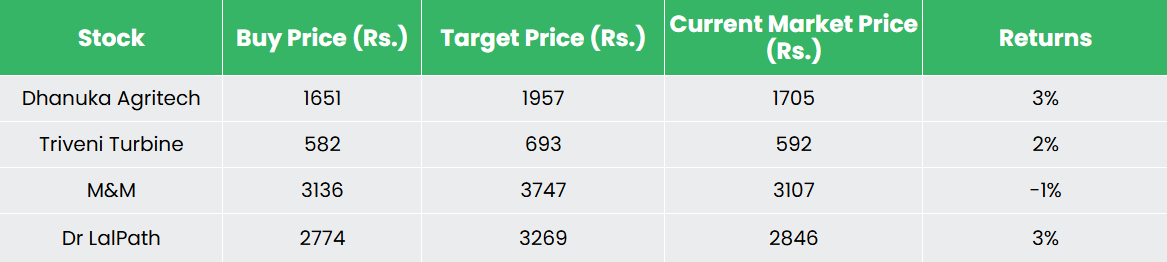

Recap of our earlier suggestions (As on 06 June 2025)

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Submit Views:

509