![MIDHANI Restricted – Evaluation, Goal Value, BUY [July 25]Insights](https://i0.wp.com/www.fundsindia.com/blog/wp-content/uploads/2025/07/Midhani-1.png?w=1920&resize=1920,960&ssl=1 "MIDHANI Restricted – Evaluation, Goal Value, BUY [July 25]Insights")

{kind=link}

Mishra Dhatu Nigam Ltd – Fostering Self-Reliance

Included in 1973 below the executive management of Ministry of Defence, Mishra Dhatu Nigam Ltd. (MIDHANI) is a longtime participant within the manufacture of particular steels, superalloys, and titanium alloys. Headquartered in Hyderabad, the corporate was setup with an goal to attain self-reliance within the provide of assorted alloys to defence and different strategic sectors corresponding to vitality, area and aeronautical functions. The corporate is the one producer of Titanium alloys in India. Recognised as a Nationwide Centre for Excellence in superior metallurgical manufacturing, the corporate has 2 manufacturing amenities positioned at Hyderabad and Rohtak.

Merchandise and Providers

The merchandise supplied by the corporate may be categorized as below:

- Superalloys – Nickel, cobalt and iron-based alloys.

- Titanium and titanium alloys – Commercially pure grades, alpha and alpha-beta titanium alloys.

- Particular metal – Martensitic steels, excessive power particular metal, austennitic steels and percipitation hardening steels.

- Different metals and alloys – Smooth magnetic alloys and managed growth alloys.

- Specialty merchandise – Wires and bars, rolled sheets, open-die forgings, funding castings, armour merchandise, biomedical implants, fasteners and so on.

Subsidiaries: As of FY24, the corporate has 1 three way partnership, and no different subsidiary/affiliate firm.

Funding Rationale

- Strategic place – The corporate performs a crucial function in advancing self-reliance in defence manufacturing by producing specialised supplies which might be sometimes imported, supporting key applications involving missiles, submarines, naval platforms, fight plane, helicopters, and armoured autos. The corporate additionally provides high-performance alloys to ISRO, supporting crucial parts of area missions, together with launch autos, satellites, and cryogenic engine methods. MIDHANI serves as a key pillar of the ‘Make in India’ initiative in high-technology metallurgy, backed by sturdy collaborations with DRDO, HAL, ISRO, BHEL, and so on. The corporate additionally possesses sturdy capabilities to develop and scale superior supplies for aerospace and vitality functions.

- Development methods – MIDHANI is strategically centered on import substitution and capability growth via indigenous innovation, having developed three grasp alloys that had been beforehand imported and actively advancing applied sciences to recycle high-value scrap supplies in collaboration with authorities businesses and nationwide labs. Efforts are underway to indigenous extra grasp alloys which might be required to make superior Titanium alloys for aerospace grade. The corporate just lately commissioned new Titanium plant which is now at full-fledged operations at a capability of 250-300 tons per thirty days. It’s also engaged on creating superior supplies for hypersonic functions and next-generation jet engines. Moreover, the corporate has begun fulfilling export orders from main international gamers corresponding to Boeing, Pratt & Whitney, Airbus, and GE. As well as, it’s engaged on the event of specialised alloys for high-megawatt thermal energy vegetation for the federal government.

- Q4FY25 – Through the quarter, the corporate’s income was flat at Rs.411 crore. The manufacturing worth elevated by 17% throughout the interval to Rs.329 crore. EBITDA improved by 16% from Rs.80 crore of Q4FY24 to Rs.93 crore of the present quarter. The corporate reported internet revenue of Rs.56 crore, a development of twenty-two% in comparison with the Rs.46 crore of the corresponding interval within the earlier 12 months.

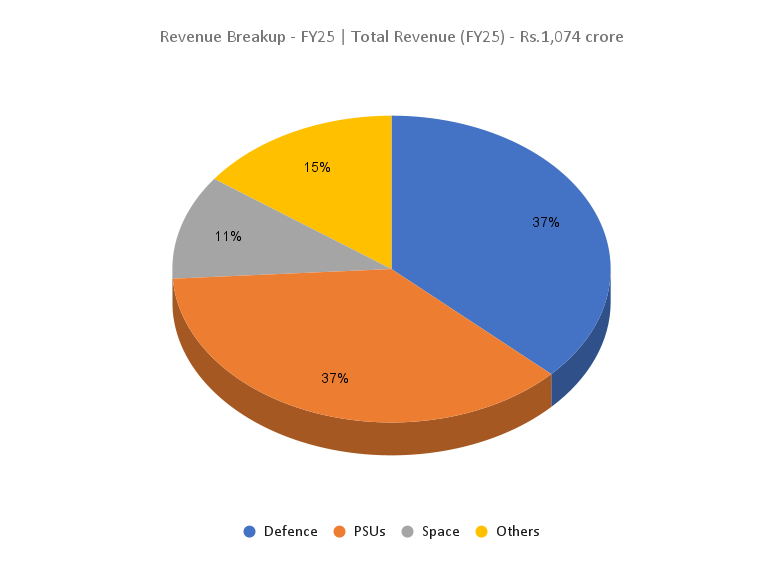

- FY25 – Throughout FY25, the income was flat at Rs.1,074 crore. EBITDA was at Rs.218 crore, up by 12% YoY. The corporate reported internet revenue of Rs.111 crore, a rise of 21% YoY. Notably, firm’s exports have elevated threefold throughout the 12 months. Through the interval the corporate has undertaken a capital expenditure of Rs.50 crore for strengthening manufacturing infrastructure and commissioning new amenities.

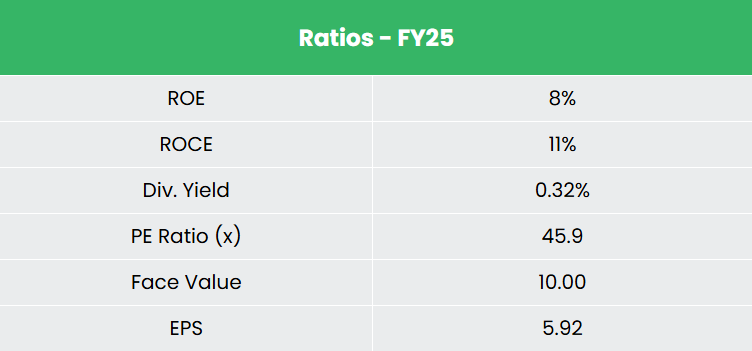

- Monetary Efficiency – Common 3-year ROE & ROCE is round 9% and 12% for FY23-25 interval. The corporate has a strong capital construction with a debt-to-equity ratio of 0.25.

Business

India’s defence and aerospace business is witnessing fast development, pushed by authorities deal with self-reliance, rising exports, and elevated R&D investments below the ‘Aatmanirbhar Bharat’ initiative. With a goal of reaching US$ 6.02 billion in annual defence exports by 2028 – 29, the sector is a strategic precedence. Successes like Chandrayaan-3 and the growth of indigenous satellite tv for pc methods (IRNSS, GSAT) spotlight technological progress, whereas the mixing of area and defence capabilities is supporting development throughout sectors corresponding to infrastructure, agriculture, and telemedicine – creating long-term alternatives for superior supplies and alloy producers.

Development Drivers

- In 2025-26 the central authorities has allotted Rs.6,81,210 crore for the Ministry of Defence which is 6% larger than the earlier 12 months.

- Provision for 100% International Direct Funding (FDI) via Authorities route and 74% via Automated route into the defence sector.

- India Area Sector’s goal to focus on exports value $11 Bn by 2033.

Peer Evaluation

Opponents: DCX Techniques Ltd, Sunflag Iron & Metal Firm Ltd, and so on.

In comparison with its friends, the corporate stands out as the biggest alloy provider to the defence sector. Its profitability metrics are passable, reflecting a secure monetary place and strong operational efficiency.

Outlook

As of 1 April 2025, MIDHANI holds a strong order e book of Rs.1,832 crore, making certain sturdy income visibility for the approaching years. The corporate is focusing on an annual development charge of 20%, supported by its deal with self-reliance in uncooked supplies via indigenous growth and recycling of high-value scrap. It goals to maintain wholesome EBITDA margins within the vary of 20 – 25%. To assist future development and technological development, MIDHANI plans to speculate Rs.75 – 100 crore yearly in capital expenditure. It anticipates elevated demand from key strategic sectors together with aerospace, naval, missile, area, and energy. With over 500 alloy grades indigenized, the corporate can be broadening its product portfolio to serve rising sectors corresponding to healthcare, oil & fuel, and vitality – enhancing its long-term development prospects whereas lowering dependency on conventional defence-led income streams.

Valuation

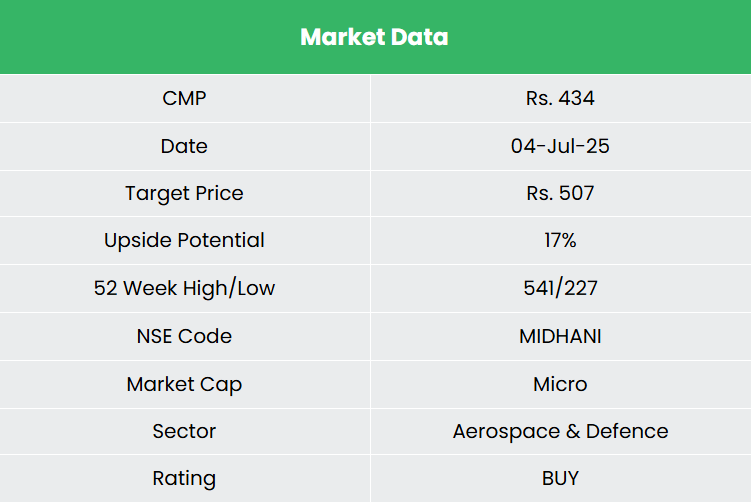

We imagine the corporate is well-positioned with a robust order pipeline, rising export presence, and ongoing growth of next-generation alloys. We advocate a BUY score within the inventory with the goal worth (TP) of Rs.507, 51x FY27E EPS.

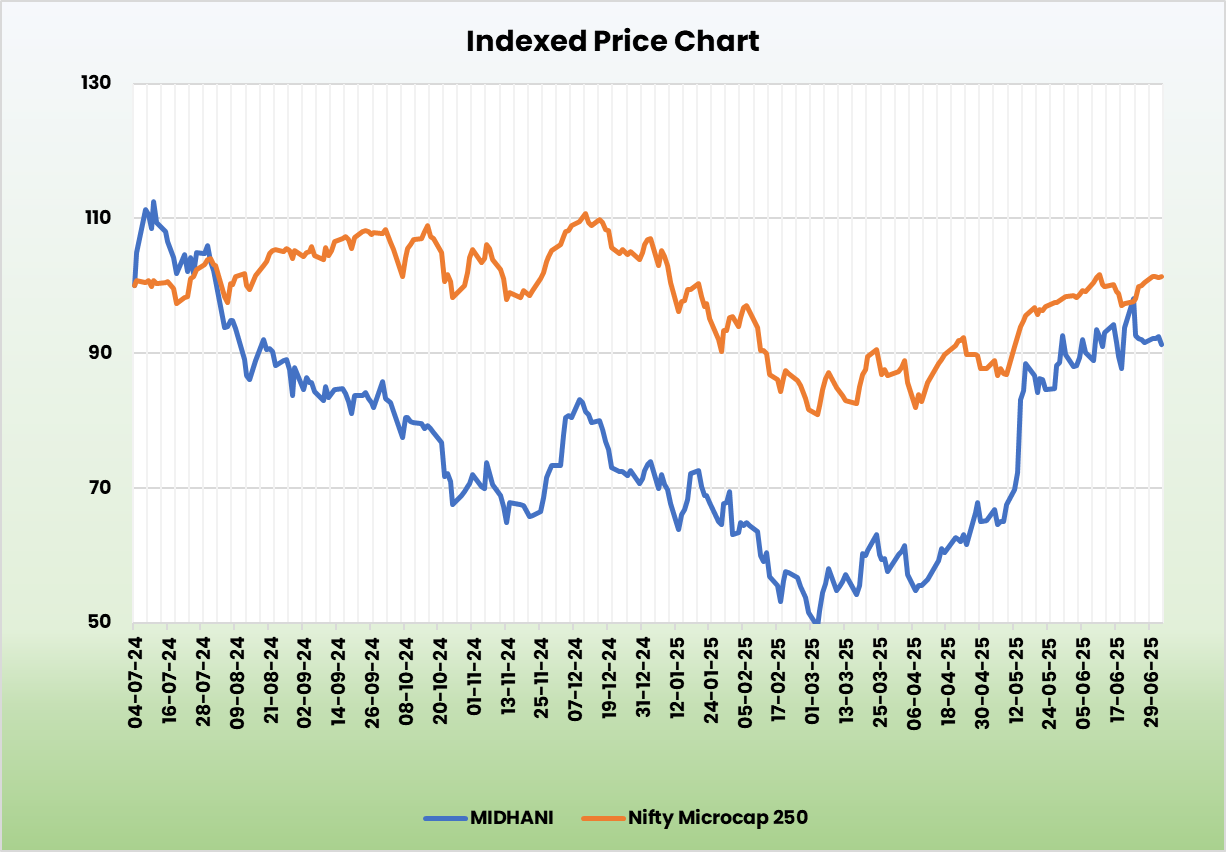

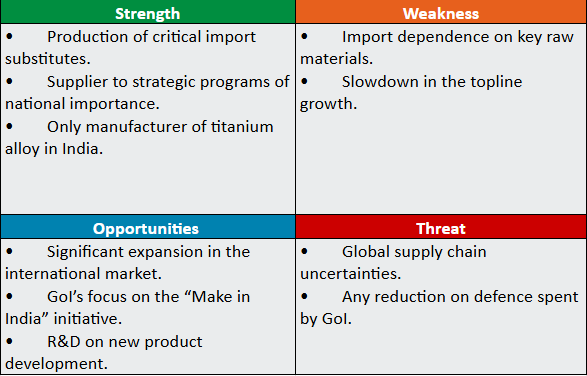

SWOT Evaluation

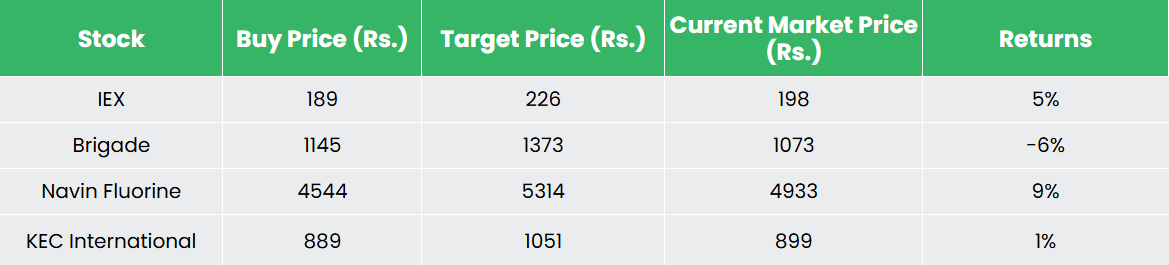

Recap of our earlier suggestions (As on 04 July 2025)

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you could like

Put up Views:

382