{kind=link}

With mortgage charges staying stubbornly elevated, new narratives are being written in an try to vary that view.

A preferred certainly one of late has been arguing that mortgage charges aren’t that top as we speak. Or not as excessive as individuals assume.

The rationale is that while you zoom out, mortgage charges are literally fairly center of the street traditionally, which bucks the misunderstanding that they’re excessive.

In any case, they had been within the excessive double-digits within the Nineteen Eighties, and nonetheless begin with a 6 as we speak. Appears okay, proper?

So is it true that mortgage charges aren’t so dangerous?

Context Is Key for Mortgage Charges

I may sit right here and inform you a similar factor. That mortgage charges aren’t that top. However what goal would that serve if the proposed month-to-month fee nonetheless doesn’t pencil?

And what solace would that present for those who knew you missed the boat on snagging a 2-3% mounted charge just some years earlier?

It in all probability wouldn’t provide you with any consolation until you’re an excessive optimist. As a substitute, you’re in all probability simply doing the maths like everybody else and never liking what you see.

For those who’re a potential residence purchaser as we speak, mortgage charges are prime of thoughts. And also you in all probability don’t care what the long-term common is for the 30-year mounted.

Spoiler alert: It’s a better 7.75%, or about 75 foundation factors (bps) above present ranges.

Does this imply the 30-year mounted is a screaming cut price as we speak? I wouldn’t say so, however others would possibly attempt to make that argument.

The most important ache level of the previous few years has been the magnitude of change in mortgage charges (going from sub-3% to 7%+ in simply over a yr).

Positive, mortgage charges sit beneath their long-term common. And surely, they’re greater than half that of the Nineteen Eighties mortgage charges, when the 30-year mounted almost cracked 19%.

However realizing that also may not change the truth that shopping for a house as we speak has fallen out of attain for a lot of.

Dwelling Purchaser Affordability Stays a Problem however Is Slowly Bettering

Maybe as a substitute of mortgage charges in a vacuum, we should always take into account general housing affordability.

In any case, mortgage charges could possibly be larger as we speak and shopping for situations extra reasonably priced, assuming residence costs had been decrease and/or wages had been larger.

Taking a holistic view permits us to scale back give attention to mortgage charges and have a look at the large image.

It additionally forces us to ask why housing is so costly as we speak, a solution that generally goes again to a scarcity of accessible provide.

There’s nonetheless a deficit of properties on the market in most markets nationwide, although it’s starting to ease some.

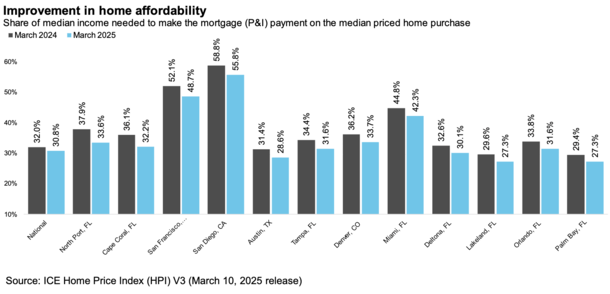

A latest report from ICE discovered that the share of median earnings required to make a principal and curiosity fee fell from 32% in March 2024 to 30.8% in March 2025.

It’s not an enormous distinction, however not less than it’s transferring in the precise path. And satirically, as pertains to this publish, it’s possible higher principally resulting from decrease mortgage charges.

In order a lot as of us need to say mortgage charges don’t matter, they do. They’re a bit decrease than they had been a yr in the past, regardless of remaining elevated.

Actually, a 1% drop in mortgage charges is the same as a ten%+ drop in properties costs. Which means it’s in all probability simpler to get charges decrease than it’s a worth correction/crash.

Particularly when there’s a scarcity of properties available on the market. Provide is de facto what drives costs, not mortgage charges.

One other Smooth Spring for Dwelling Shopping for On account of Excessive Mortgage Charges?

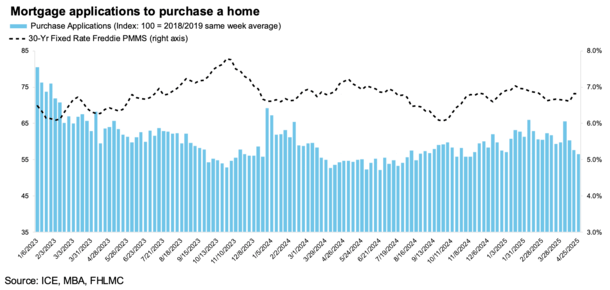

A unique report from ICE from Might discovered that residence buy purposes haven’t risen as a lot as one would count on for this time of the yr.

We’re principally at peak residence shopping for season and regardless of many YoY good points in weekly mortgage purposes, the numbers simply aren’t there (additionally recall 2024 residence gross sales had been the worst since 1995).

By means of April twenty fifth, purposes rose in every of the prior 13 weeks, however had been solely up 3% YoY within the week of April twenty fifth.

ICE famous that it’s “a a lot decrease charge of development than the standard +9% to +24% anticipated” throughout this time of the yr.

So even when mortgage charges “aren’t that top,” mixed with the place residence costs and wages are, they seem like cost-prohibitive.

The proof is that residence buy apps “spiked within the speedy aftermath of reciprocal tariff bulletins in early April” when mortgage charges quickly dipped.

So it’s clear charges nonetheless matter, quite a bit. And if/once they go down, residence consumers are inclined to pounce.

On the similar time, one may argue that the artificially low mortgage charges seen over a lot of the previous decade masked different points like eroding affordability resulting from quickly ascending residence costs and a scarcity of accessible provide.

We primarily acquired away with it whereas mortgage charges ran at greater than 50% off their historic, long-term common.

However now that charges are again to “regular,” the maths merely ain’t mathing.

Learn on: The Trick Dwelling Builders Use to Promote Extra Properties

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Observe me on X for warm takes.