{kind=link}

The Authorities of India rolled out the Nationwide Pension Scheme (NPS) for all of the residents of India manner again on Could 1, 2009 and for company sector from December, 2011. Since then, NPS has turn into one of the crucial widespread funding and tax saving choices in India.

The numbers converse for themselves – The Complete belongings underneath administration (AUM) with NPS is now at Rs. 8.82 Lakh crore with Y-o-Y development of 23.45%. The variety of subscribers underneath numerous schemes underneath the Nationwide Pension System (NPS) rose to 624.81 lakh as at March 4th 2023 from 508.47 Lakh in March 2022 displaying a year- on- 12 months (Y-o-Y) improve of twenty-two.88%.

Most of my weblog readers have chosen NPS for 2 principal causes – i) for tax saving objective & ii) No different alternative however to take a position, as contribution to NPS has been made obligatory for a lot of the Govt staff.

If you’re investing in NPS Scheme or planning to spend money on NPS, you want to concentrate on all the newest NPS Earnings Tax advantages which are at present out there underneath outdated Tax Regime and New Tax Regime (w.e.f FY 2020-21).

On this submit, lets talk about – What are the NPS Earnings Tax advantages for FY 2023-24 or AY 2024-25? Are you able to declare Earnings Tax Deduction on NPS contribution underneath New Tax Regime? Are there any tax deductions underneath NPS Tier-2 account? Beneath what sections of the IT act NPS investments may be claimed as tax deductions? What’s the funding proof to avail the tax profit underneath NPS for FY 2023-24?

Newest NPS Earnings Tax Advantages FY 2023-24 / AY 2024-25 underneath Outdated & New Tax Regimes

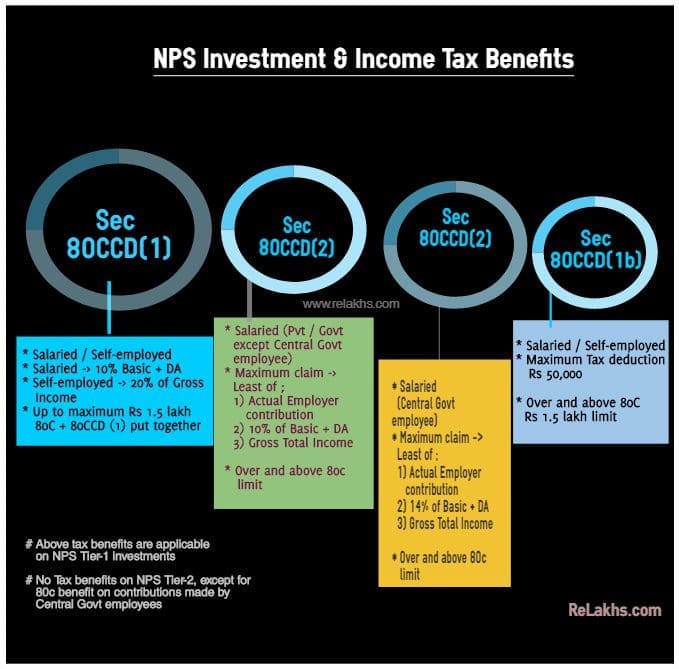

Beneath are the assorted Earnings Tax Sections underneath which an NPS investor can declare Earnings Tax Deductions for FY 2023-24 / AY 2024-25 .

- Part 80C

- Part 80CCD (1)

- U/S 80CCD (1b)

- Part 80CCD (2)

“Beneath the brand new tax regime, the primary three deductions should not out there, however the fourth one continues to be out there”

Earnings Tax Advantages underneath NPS Tier-1 Account for AY 2024-25

Tax Deduction underneath 80CCD(1) on NPS funding by Salaried particular person (besides Central Govt staff) :

- An Worker can contribute to Authorities notified Pension Schemes (like Nationwide Pension Scheme – NPS). The contributions may be upto 10% of the wage (salaried people).

- The utmost quantity that may be claimed as tax deduction is Rs 1.5 lakh u/s 80 CCD(1).

Outdated Tax Regime : If you’re opting outdated tax regime then you may proceed claiming earnings tax deduction as listed within the above two factors.

New Tax Regime : If you’re going forward with New Tax Regime then you can’t declare earnings tax advantages u/s 80 CCD(1).

Tax Deduction underneath 80CCD(1) on NPS funding by Self-employed particular person :

- The self-employed (particular person aside from the salaried class) can contribute as much as 20% of their gross earnings and the identical may be deducted from the taxable earnings underneath Part 80CCD (1) of the Earnings Tax Act, 1961.

- The utmost quantity that may be claimed as tax deduction is Rs 1.5 lakh u/s 80CCD(1).

Beneath Outdated Tax Regime : If you’re opting outdated tax regime then you may proceed claiming earnings tax deduction as listed within the above two factors.

New Tax Regime : If you’re going forward with New Tax Regime then you definately can’t declare earnings tax advantages u/s 80CCD(1).

Earnings Tax Deduction underneath 80CCD(2) on NPS funding for Non-Central Govt Staff :

- An employer may contributes to NPS scheme.

- The contribution quantity made by the employer may be claimed as tax deduction u/s 80CCD(2), topic to the brink restrict of, least of the beneath; Quantity contributed by an employer

- 10% of Primary wage + DA (or)

- Gross Complete earnings

- That is a further deduction which won’t kind a part of Sec.80C restrict.

- Self-employed people should not eligible to say the NPS tax deduction u/s 80CCD(2).

Beneath outdated & New Tax Regime : If you’re choosing New Tax Regime in your Earnings Tax Return then there’s now a threshold restrict u/s 80CCD(2), with efficient from FY 2020-21. Your employer can contribute to your NPS account as talked about within the above factors. Nonetheless, in case your employer’s contributions underneath Sec 80CCD(2) are greater than Rs 7,50,000 a 12 months (together with EPF and Superannuation), then such exceeding contributions are taxable earnings within the palms of the worker. The curiosity earned on over and above Rs 7.5 lakh steadiness can be taxable.

Earnings Tax Deduction underneath 80CCD(2) on NPS funding for Central Govt Staff :

- The contribution quantity made by the employer (Central Govt on this case) may be claimed as tax deduction u/s 80CCD(2), topic to the brink restrict of, least of the beneath;Quantity contributed by an employer

- 14% of Primary wage + DA (or)

- Gross Complete earnings

- The Centre will now contribute 14% of primary wage to Govt staff’ pension corpus, up from 10%. That is w.e.f April 2019.

- That is a further deduction which won’t kind a part of Sec.80C restrict.

Beneath outdated & New Tax Regime : If you’re choosing New Tax Regime in your Earnings Tax Return then there’s now a threshold restrict u/s 80CCD(2), with efficient from FY 2020-21. Your employer can contribute to your NPS account as talked about within the above factors. Nonetheless, in case your employer’s contributions underneath Sec 80CCD(2) are greater than Rs 7,50,000 a 12 months (together with EPF and Superannuation), then such exceeding contributions are taxable earnings within the palms of the worker. The curiosity earned on over and above Rs 7.5 lakh steadiness can be taxable.

NPS Extra Tax Deduction u.s 80CCD(1b)

An extra tax advantage of Rs 50,000 may be claimed u/s 80CCD (1b) by the salaried or self-employed people.

Kindly be aware that the Complete Deduction underneath part 80C, 80CCC and 80CCD(1) collectively can’t exceed Rs 1,50,000 for the monetary 12 months 2020-21. The extra tax deduction of Rs 50,000 u/s 80CCD (1b) is over and above this Rs 1.5 Lakh restrict.

Beneath Outdated Tax Regime : If you’re opting outdated tax regime then you may proceed claiming earnings tax deduction of Rs 50,000 u/s 80CCD(1b).

New Tax Regime : If you’re going forward with New Tax Regime then you definately can’t declare further earnings tax deduction of Rs 50,000 u/s 80CCD(1b).

Earnings Tax Advantages underneath NPS Tier-2 Account for FY 2023-24

The Tier II Nationwide Pension Scheme account is rather like a financial savings account and subscribers are free to withdraw the cash as and at any time when they require.

Tax Deduction underneath 80c for NPS Tier-2 funding

The contributions by the federal government staff (solely) underneath Tier-II of NPS will probably be lined underneath Part 80C for deduction as much as Rs 1.5 lakh for the aim of earnings tax, with a three-year lock-in interval. That is w.e.f April, 2019.

For different NPS subscribers, there aren’t any tax advantages out there on NPS investments in Tier-2 accounts.

Beneath Outdated Tax Regime : If you’re opting outdated tax regime then you may proceed claiming earnings tax deduction u/s 80C.

New Tax Regime : If you’re going forward with New Tax Regime then you definately can’t declare these contributions u/s 80c.

NPS Maturity Proceeds & Withdrawal Guidelines FY 2023-24

Beneath are the frequent guidelines which are relevant underneath outdated and new tax regimes concerning NPS Maturity proceeds and withdrawals;

NPS Tier-1 Maturity proceeds on Retirement is Tax-exempt

- After attaining 60 years of age, you’re allowed to withdraw 60% of the entire Corpus quantity and no less than 40% of the accrued wealth within the NPS account must be utilized for buy of annuity/pension plan.

- With efficient from 1st April, 2019, the 60% NPS withdrawal is absolutely tax-exempt.

- In case the entire corpus within the account is lower than Rs. 2 Lakhs as on the Date of Retirement (Authorities sector)/attaining the age of 60 (Non-Authorities sector), the subscriber (aside from Swavalamban subscribers) can avail the choice of full withdrawal. Nonetheless 60% of this withdrawal will probably be tax-exempt and 40% is taxable.

NPS Tier-1 Account & Partial withdrawals

The Tier 1 account is non-withdrawable until the particular person reaches the age of 60. Nonetheless, partial withdrawal earlier than that’s allowed in particular circumstances.

- Within the newest rule change (Price range 2017), PFRDA (Pension Fund Regulatory And Improvement Authority) has relaxed the withdrawal norms to the impact that now the subscribers can withdraw as much as 25% of contributions ranging from the third 12 months of opening of NPS.

- Kindly be aware that such partial withdrawals are tax-exempt. (The NPS partial withdrawals made earlier than 1.04.2017 are taxable.)

The withdrawals from NPS Tier 2 account don’t include any earnings tax profit. The tax assessee is accountable for taxation on any beneficial properties arising out of investments in NPS Tier-II account and such beneficial properties are taxable as per the relevant earnings tax slab charges.

Can NRIs declare Tax deductions on NPS AY 2024-25?

Whether or not you’re eligible to say tax advantages relies on the tax regime you go for for FY 2023-24.

Non-resident Indians (NRIs) are eligible to spend money on the NPS scheme identical to resident Indians. The Rs 50,000 further tax profit on NPS can be out there to NRIs. These tax deductions can be found underneath outdated tax regime.

The switch of funds must be routed by way of a non-resident exterior account (NRE) or non-resident peculiar account (NRO). The one distinction is that the previous is a repatriable resident account whereas the latter is non-repatriable one.

What’s the funding proof to avail the tax profit underneath NPS?

The Subscriber can submit the Transaction Assertion as an funding proof. Alternatively, Subscriber from “All Residents of India” may obtain the receipt of voluntary contribution made in Tier I account for the required monetary 12 months from NPS account NSDL log-in. It may be downloaded from the sub menu “Assertion of Voluntary Contribution underneath Nationwide Pension System (NPS)” out there underneath principal menu “View” in NPS account log-in.

Kindly be aware that this text is not a suggestion to spend money on NPS Scheme. It is just meant to supply info on NPS Earnings tax advantages FY 2023-24.

Proceed studying:

(Publish first revealed on : 23-Sep-2023)