{kind=link}

Firm overview

NTPC Inexperienced Vitality Restricted (NGEL) is the most important renewable vitality public sector enterprise (excluding hydro) by way of working capability as of 30 September 2024. It’s the wholly owned subsidiary of NTPC Restricted, a ‘Maharatna’ central public sector enterprise. The corporate’s renewable vitality portfolio includes of each photo voltaic and wind energy property with presence throughout a number of places in additional than 6 states. The corporate has an operational capability of three,220 MW of photo voltaic tasks and 100 MW of wind tasks throughout six (6) states as of 30 September 2024. The corporate’s mission portfolio consisted of 16,896MWs together with 3,320 MWs of working tasks and 13,576 MWs of contracted and awarded tasks.

Objects of the supply

- To spend money on the corporate’s wholly owned subsidiary NTPC Renewable Vitality Restricted (NREL) for compensation/ prepayment, in full or in a part of sure excellent borrowings availed by NREL; and

- Basic company functions.

Funding Rationale

- Sturdy parentage – The corporate advantages from the sturdy backing of NTPC Restricted, a significant built-in vitality participant with an electrical energy technology capability of 76 GW (as of 30 September 2024), spanning coal, hydro, fuel, and renewable vitality operations throughout India. NTPC Ltd brings intensive experience in executing large-scale tasks, sturdy long-term relationships with offtakers and suppliers, and vital monetary power. NGEL is poised to play an important function in NTPC’s technique to develop its non-fossil-based capability to 45-50% of its portfolio, with a goal of 60 GW in renewable vitality capability by 2032. Moreover, NGEL additional derives advantages from NTPC by way of its expertise in environment friendly operations of energy stations, superior execution capabilities, land banks throughout India for energy tasks, expertise of coping with State DISCOMs and so on. NGEL additionally holds the best credit standing from CRISIL, reflecting the sturdy credit score profile of its mum or dad, NTPC Restricted.

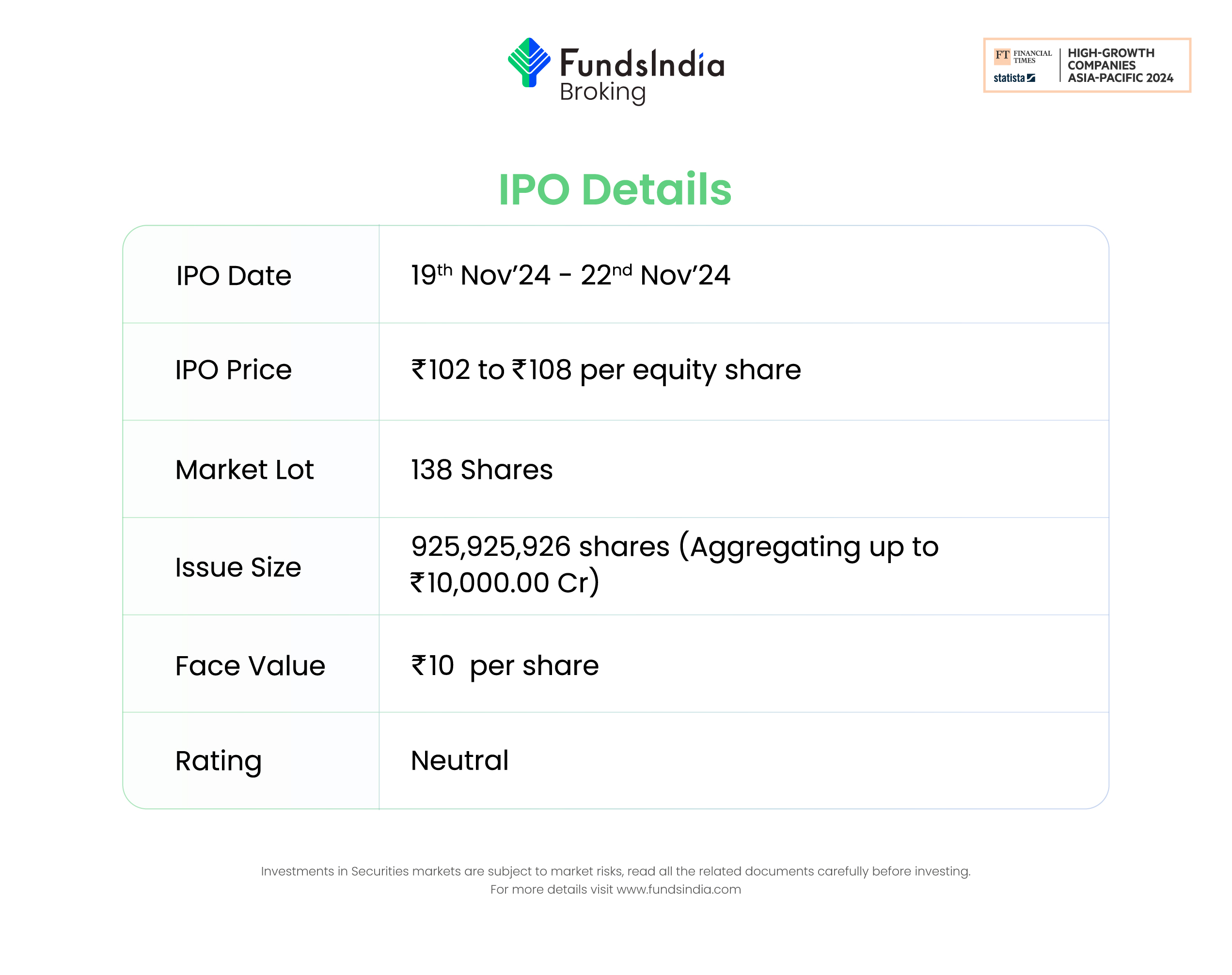

- Established place – The corporate ranks among the many high 10 renewable vitality gamers in India by operational capability. It boasts a considerable portfolio of utility-scale photo voltaic and wind vitality tasks, serving each public sector undertakings (PSUs) and Indian corporates. As of 30 September 2024, the portfolio totaled 16,896 MW, together with 3,320 MW from working tasks and 13,576 MW from contracted and awarded tasks. The pipeline capability stood at 9,175 MW, bringing the mixed whole of the portfolio and pipeline to 26,071 MW. The corporate has 17 offtakers throughout 41 photo voltaic tasks and 11 wind tasks, all of that are authorities businesses and public utilities, with long-term Energy Buy Agreements (PPAs) which have a mean time period of 25 years.

- Monetary efficiency – The corporate reported income of Rs.1,963 crore in FY24 towards Rs.170 crore in FY23, a development of 1057%. The EBITDA of the corporate in FY24 is at Rs.1,747 crore, a 1054% YoY development in comparison with the Rs.151 crore of FY23. The online revenue elevated by 101% in comparison with Rs.345 crore in comparison with Rs.171 crore of FY22.

Key dangers

- Uncooked materials worth volatility – Any disruption to the well timed and ample provide, or volatility within the costs of required supplies, elements and gear might adversely impression on the enterprise, outcomes of operations and monetary situation.

- Regional focus – A significant portion of the corporate’s renewable vitality tasks are concentrated in Rajasthan (62% as of 30 September 2024). Any vital social, political, financial or seasonal disruption, pure calamities or civil disruptions in Rajasthan might have an antagonistic impact on the enterprise.

Outlook

We consider that the backing of the NTPC Group will allow NGEL to develop its renewable vitality portfolio and set up itself as a number one inexperienced energy firm in India. The corporate’s technique to develop its mission pipeline by means of cautious bidding and strategic partnerships with PSUs and personal corporates, together with its concentrate on rising vitality options equivalent to inexperienced hydrogen, inexperienced chemical substances, and vitality storage, positions it for vital development. Moreover, the chance to contribute to the nation’s sustainability objectives additional enhances the corporate’s development potential. In accordance with RHP, Adani Inexperienced Vitality Restricted and ReNew Vitality World PLC are the listed rivals for NGEL. The friends are buying and selling at a mean P/E of 153.44x with the best P/E of 259.83x and the bottom being 47.05x. On the greater worth band, the itemizing market cap of NGEL can be round ~Rs.91,000 crore and the corporate is demanding a P/E a number of of 263.98x primarily based on put up situation diluted FY24 EPS of Rs.0.41. Primarily based on the above views, we consider the difficulty is aggressively priced (learn as overvalued) and we offer a ‘Impartial’ score for this IPO for a medium to long-term Holding.

Observe: Please word that this isn’t a suggestion and is meant just for instructional functions. So, kindly seek the advice of your monetary advisor earlier than investing.

Different articles it’s possible you’ll like

Publish Views:

160