{kind=link}

PG Electroplast Ltd – Experience meets innovation

PG Electroplast Restricted (PGEL), a flagship of PG Group, is a number one digital manufacturing service supplier in India. Based in 2003 and based mostly in Larger Noida, PGEL makes a speciality of ODM, OEM, contract manufacturing, and plastic molding. The corporate presents complete options from design to manufacturing, specializing in room air conditioners, washing machines, and plastic molding. With 10 manufacturing models and over 3,500 staff, PGEL has served 107 shoppers as of FY24 together with Astral, Blue Star, Godrej, Whirlpool, and so forth.

Merchandise and Providers

The services and products provided by the corporate could be categorized as under:

- Merchandise – Contains RAC (indoor models, out of doors models), window air conditioners, washing machines, air coolers & televisions.

- Plastics – Plastic moulding options for sanitaryware, shopper durables, automotive, shopper electronics, and so forth.

- Electronics – Electronics manufacturing comprising televisions and PCB assemblies.

- Device manufacturing – Device manufacturing for shopper durables, sanitaryware, automotive, and so forth.

Subsidiaries: As of FY24, the corporate has 2 subsidiaries and 1 three way partnership.

Progress Methods

- PG Electroplast (PGEL) started operations at a brand new AC manufacturing facility in Rajasthan, with an annual capability of 360,000 break up ACs and 250,000 window ACs, making it the second-largest ODM for RACs in India.

- The corporate plans to additional broaden AC capability and is organising a brand new built-in unit, alongside a greenfield washer facility in Larger Noida.

- PGEL has allotted Rs.370-380 crore for FY25 capex, together with Rs.125-130 crore for RACs, Rs.35-40 crore for laundry machines, and Rs.180 crore for land and buildings.

- The “Merchandise Phase” contributed 75% of Q1FY25 income, pushed by room ACs, washing machines, and air coolers, with a 60% progress goal for FY25 to Rs.2,650 crore.

- PGEL goals to boost its month-to-month manufacturing capability for indoor and out of doors AC models and double the capability of window ACs and washing machines.

Monetary Efficiency

Q1FY25

- Report-high quarterly gross sales and income in Q1FY25.

- Income grew 95% YoY to Rs.1,321 crore (vs. Rs.678 crore in Q1FY24).

- RAC enterprise elevated by 130%; the washer section rose by 72%.

- EBITDA surged 101% YoY to Rs.135 crore (vs. Rs.67 crore).

- Web revenue elevated 151% YoY to Rs.85 crore (vs. Rs.34 crore).

FY24

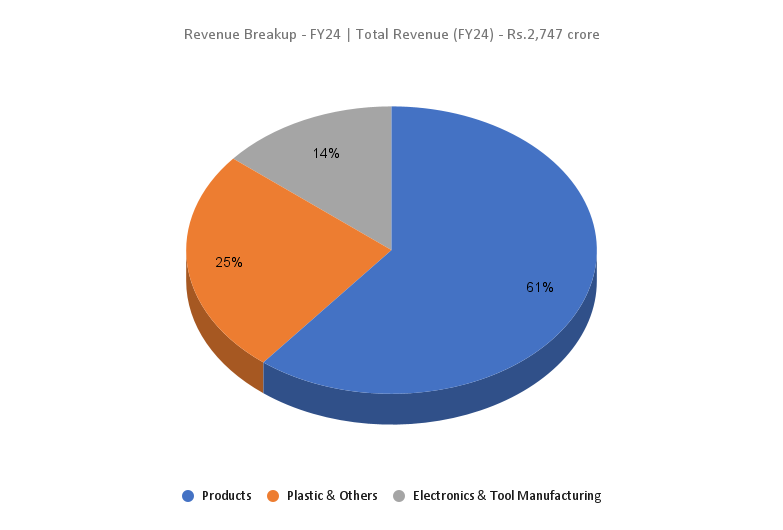

- FY24 income reached Rs.2,747 crore, up 27% YoY.

- Product enterprise contributed 60.7% to total gross sales.

- Working revenue elevated by 53% YoY to Rs.275 crore.

- Web revenue grew 78% YoY to Rs.137 crore.

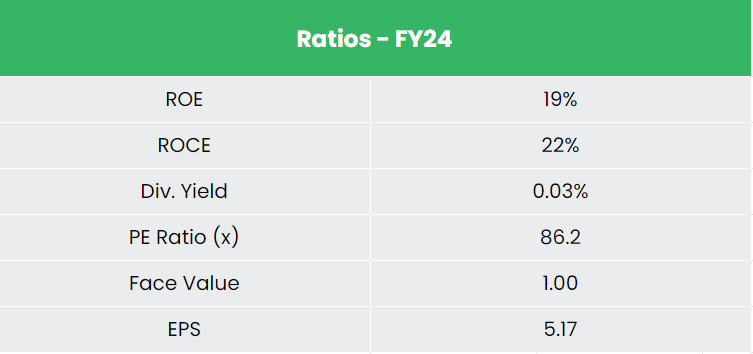

Monetary Efficiency (FY21-24)

- Income and PAT CAGR of 57% and 125% from FY 21-24.

- Common 3-year ROE of 19% and ROCE of 16%.

- Debt-to-equity ratio stands at 0.42.

Business outlook

- India’s electronics ecosystem is experiencing fast progress throughout varied sectors like mobiles, telecom, and auto electronics.

- Key progress drivers embody a rising center class, growing disposable earnings, and rising shopper demand.

- The federal government initiatives the Indian electronics manufacturing sector to achieve US$ 500 billion by 2030.

- Air conditioner market measurement is predicted to develop from 65 lakh models in 2019 to 165 lakh models by 2025.

- The Indian washing home equipment market is projected to develop from US$ 3.76 billion to US$ 5.43 billion by 2029, with a CAGR of seven.65%.

- The white items market is predicted to exceed US$ 21 billion by 2025, increasing at a CAGR of 11%. Home manufacturing contributes round US$ 4.6 billion yearly.

Progress Drivers

- 100% FDI permitted in electronics {hardware} manufacturing.

- The Indian authorities distributed Rs.79 crore (US$ 9.51 million) in fiscal incentives underneath the PLI scheme for white items in This autumn FY24.

- Key authorities initiatives like “Digital India” and “Make in India” have streamlined the method of organising manufacturing models in India.

Aggressive Benefit

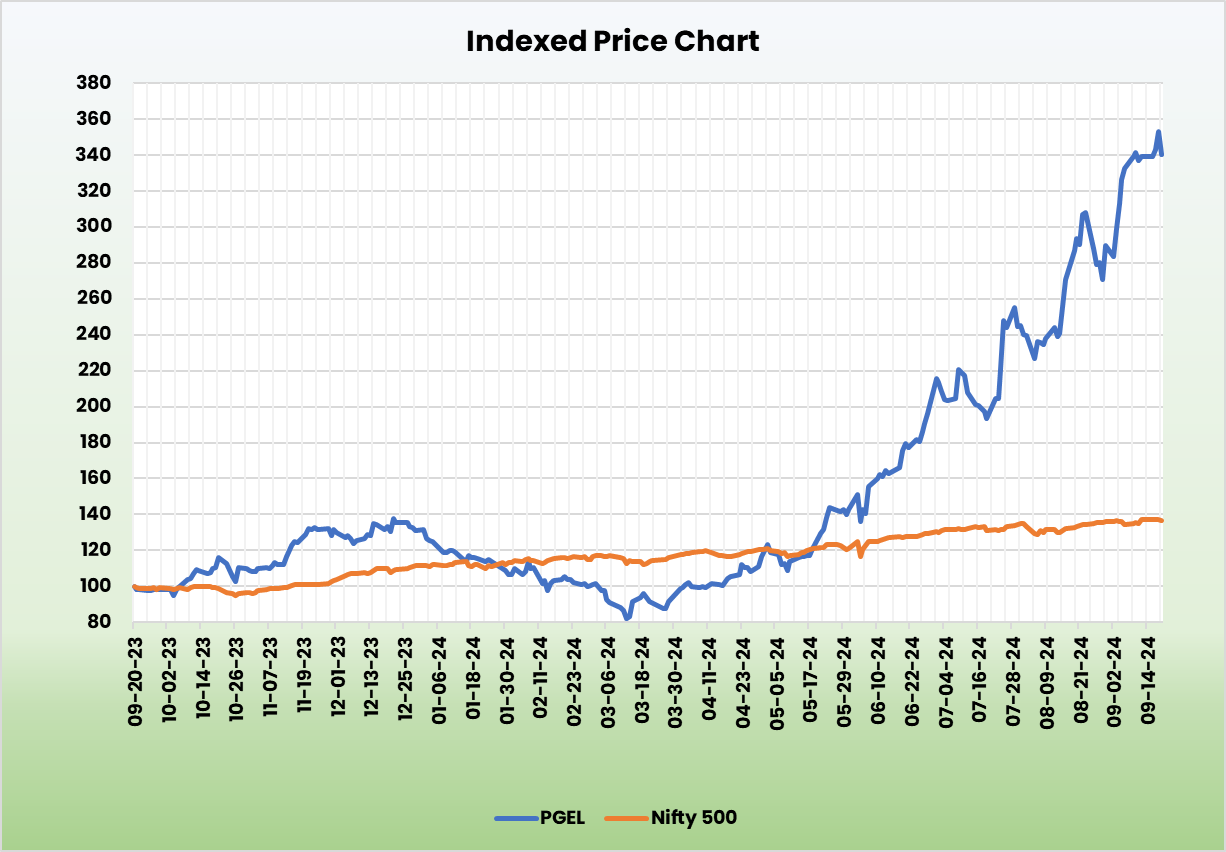

PGEL stands out as essentially the most undervalued inventory in comparison with opponents like Dixon Applied sciences and Amber Enterprises. Regardless of its decrease valuation, PGEL presents wholesome returns on capital employed and demonstrates sturdy gross sales progress, making it a powerful participant within the electronics manufacturing sector.

Outlook

- PGEL goals to be a world chief in electronics manufacturing for shopper durables and electronics.

- Shaped a three way partnership, Goodworth Electronics Restricted, in FY24 to spice up its TV and {hardware} enterprise.

- Revised FY25 working income steering to Rs.3,650 crore for PGEL and Rs.600 crore for the JV, totaling Rs.4,250 crore—up 55% from FY24.

- Projected internet revenue of Rs.216 crore in FY25, representing a 58% improve YoY.

- Expects Rs.36 crore from PLI and state incentives in FY25 and is exploring participation in PLI 2.0 for white items and PLI for IT & {Hardware}.

Valuation

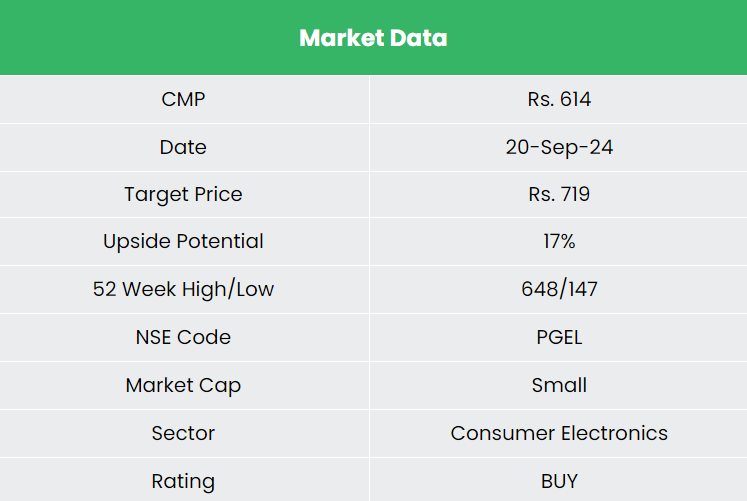

PGEL’s growth methods and the administration’s revised upward steering, we stay constructive on the corporate’s future progress prospects. We advocate a BUY score within the inventory with the goal value (TP) of Rs.719, 69x FY26E EPS.

Dangers

- Seasonality Threat: Unfavorable summer time climate could weaken demand for room air conditioners (RACs).

- Outsourcing vs Insourcing: Rising in-house manufacturing by OEMs might stress the corporate’s order ebook.

Notice: Please notice that this isn’t a suggestion and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

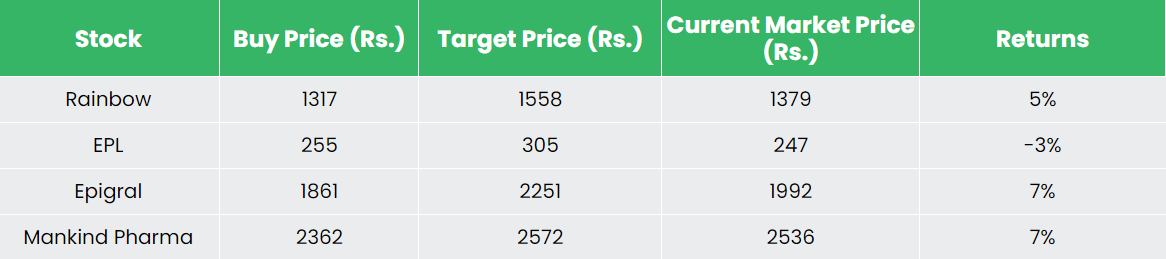

Recap of our earlier suggestions (As on 20 September 2024)

Different articles it’s possible you’ll like

Publish Views:

203