")

Administration abstract:

If you’re in search of actionable funding insights, you’ll be able to skip this put up. This put up is extra about satisfying my very own curiosity why the 2 UK traded battery funds have been doing so badly within the latest months. Within the unlikely case you have an interest in that, I invite you to learn on.

The UK was for a while a lighthouse nation for rolling out “grid scale” Battery Power Storage Techniques (BESS) in Europe. Comparatively benign regulation and help schemes allowed a big quantity of BESS capability to be developed within the UK, nicely forward of different European international locations.

UK being the UK, there was additionally an early supply for traders to take part on this growth with 2 closed finish funds/belief, One from Gresham Home (GRID( and one other one from Gore Road (GSF).

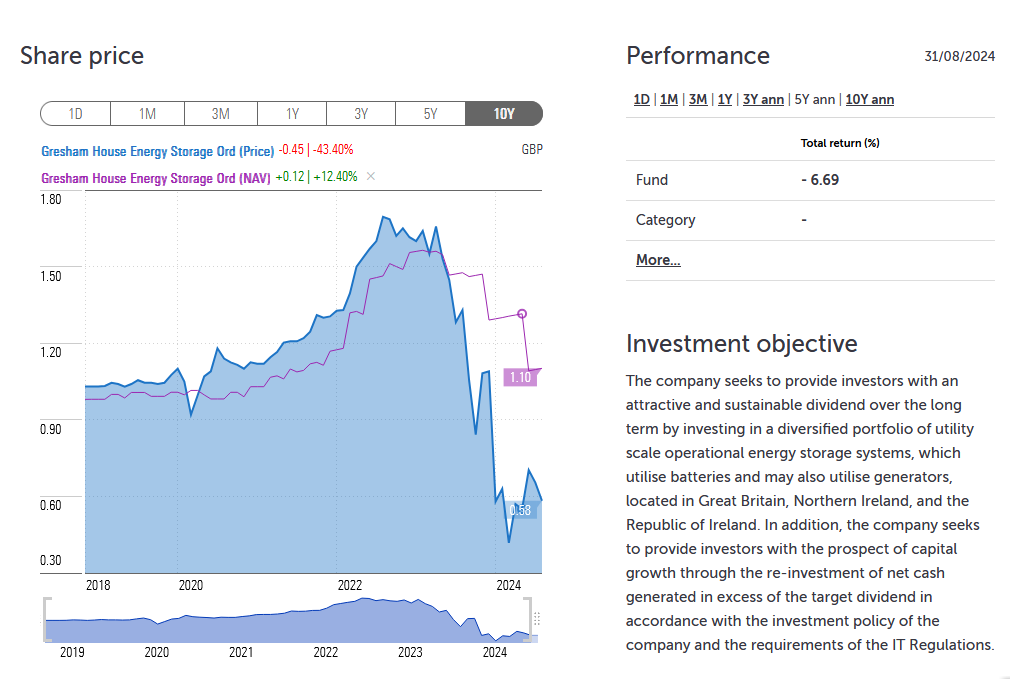

Each funds did very nicely to start with till mid 2023 earlier than declining considerably:

")

Gresham Home Power Storage fund (GRID)

The bigger of the 2, the Gresham Home Power Storage Fund with the good Ticker GRID was doing very nicely initially, with a strongly rising NAV and unit value. From inception in 2019 till mid 2023, the belief was truly buying and selling at a premium to NAV earlier than issues went south as we are able to see on this chart:

This after all results in the query: What occurred right here ?

Battery storage nonetheless is meant to be a really “scorching” asset class and an important a part of a nicely functioning Renewable Power system. Sure, the pendulum has swung again from the wild optimism following the Russian assault on Ukraine, however that doesn’t clarify the unhealthy elementary efficiency of the fund with a quickly declining NAV.

So let’s take a look at the latest historical past of the fund:

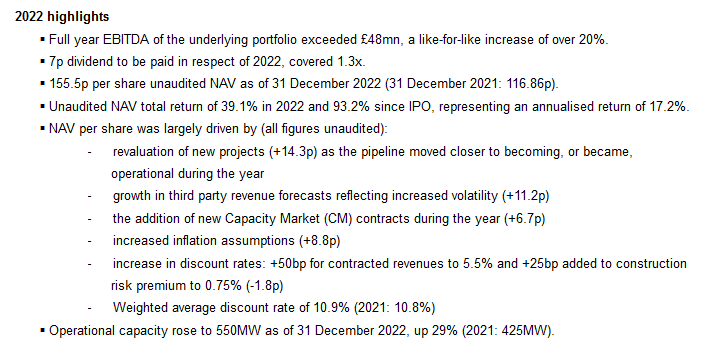

Issues seemed dandy on the finish of 2022. That is from the 12 months finish buying and selling replace:

Money was gushing in, NAV was rising considerably and everybody was comfortable. Simply as a really crude measure we are able to divide the realized EBITDA (48mn) by the common operational capability (550+435)/2 and get to plenty of ~97k EBITDA for each MW put in which appears to be like like a reasonably respectable return on funding.

Then a number of issues occurred: First, the fund positioned extra items into the market, particularly additionally for retail traders on the juicy NAV of 155 pence.

Then, the Fund supervisor Gresham Home itself was offered to an organization referred to as Searchlight Capital Companions in July 2023. The Battery fund was solely 10% of the belongings, however clearly one of the “attractive” elements.

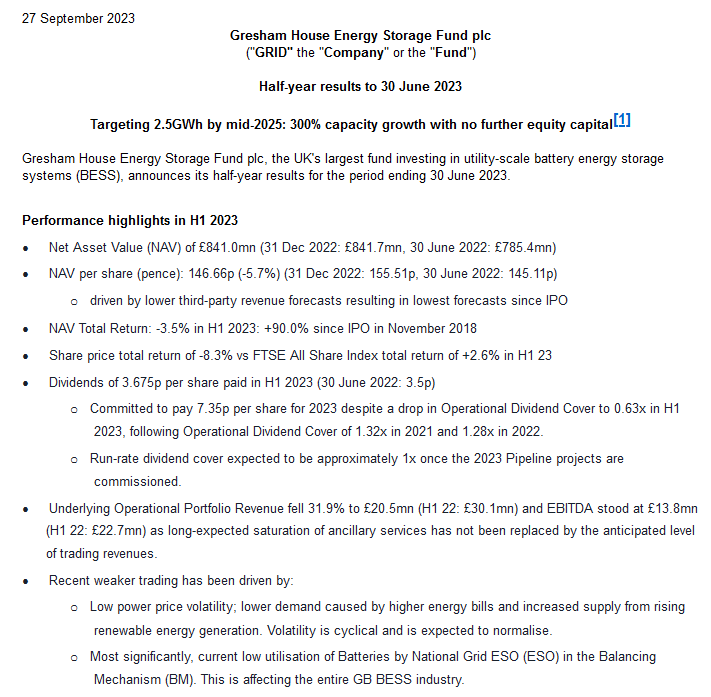

Then, coincidently solely 2 months later, within the 6M buying and selling replace, the primary cracks confirmed already with a slight discount within the NAV after a protracted sequence of will increase:

Annualized EBITDA was ~28 mn GBP, this interprets to round 49K EBITDA per MW put in. a reasonably drastic decline from simply 6 months earlier.

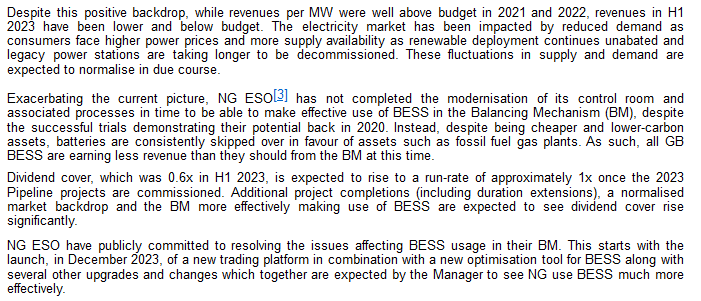

On this replace additionally they talked about for the primary time, that nationwide Grid, the operator of the UK electrical energy grid was unable (or unwilling) to incorporate BESS capability within the Grid rebalancing mechanism.

However, administration was fairly optimistic that this was solely a short lived drawback:

This optimism nevertheless was gone after they dropped the This autumn buying and selling replace in January 2024:

The Dividend was suspended.

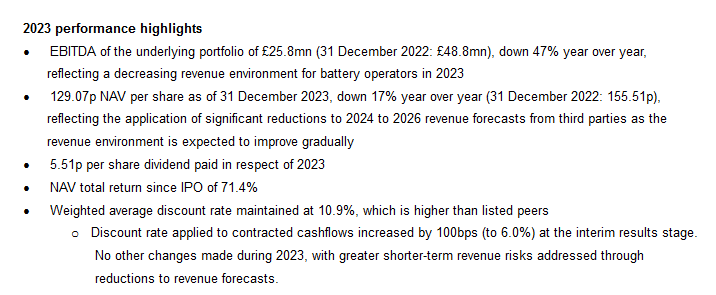

The full 12 months outcomes that have been launched in April 2024 painted a fair worse image than mid 2023:

This interprets into ~42k EBITDA per MW, a lot decrease than within the first 6M anuualized. With a valuation of ~900k per mW it was additionally clear that additional nAV cuts have been inevitable.

Quick ahead to the newest buying and selling replace, 6M 2024:

EBITDA has fallen additional, annualized EBITDA of 20,8 mn examine to on common 730 mn put in capability, giving us ~35K EBITDA per MW put in.

Administration is as soon as once more optimistic, however given the monitor document, Traders appear to be very cautious.

The Gore Road Fund

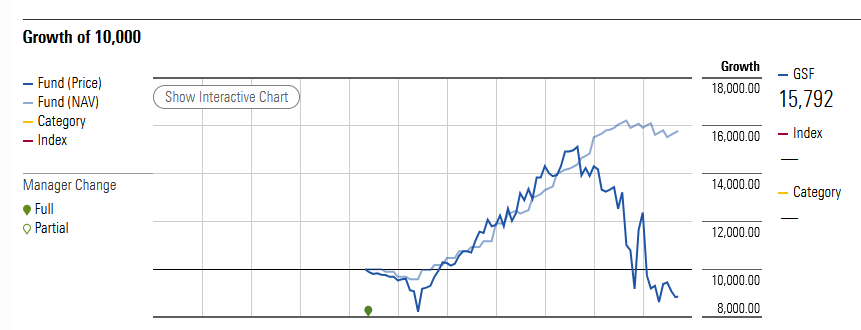

Wanting on the chart, the Gore Road fund has been doing barely higher however not that a lot:

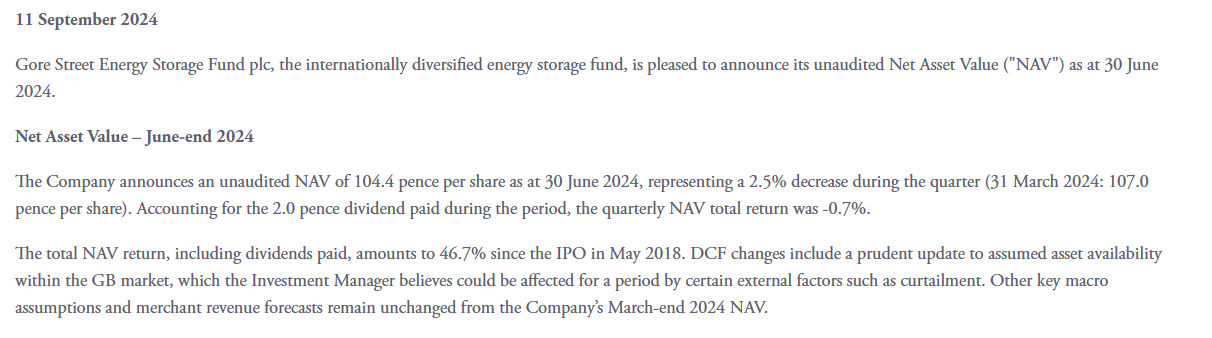

Wanting on the final buying and selling replace, they nonetheless are paying a dividend and preserve the NAV fixed, however shareholders appear to be scared, too:

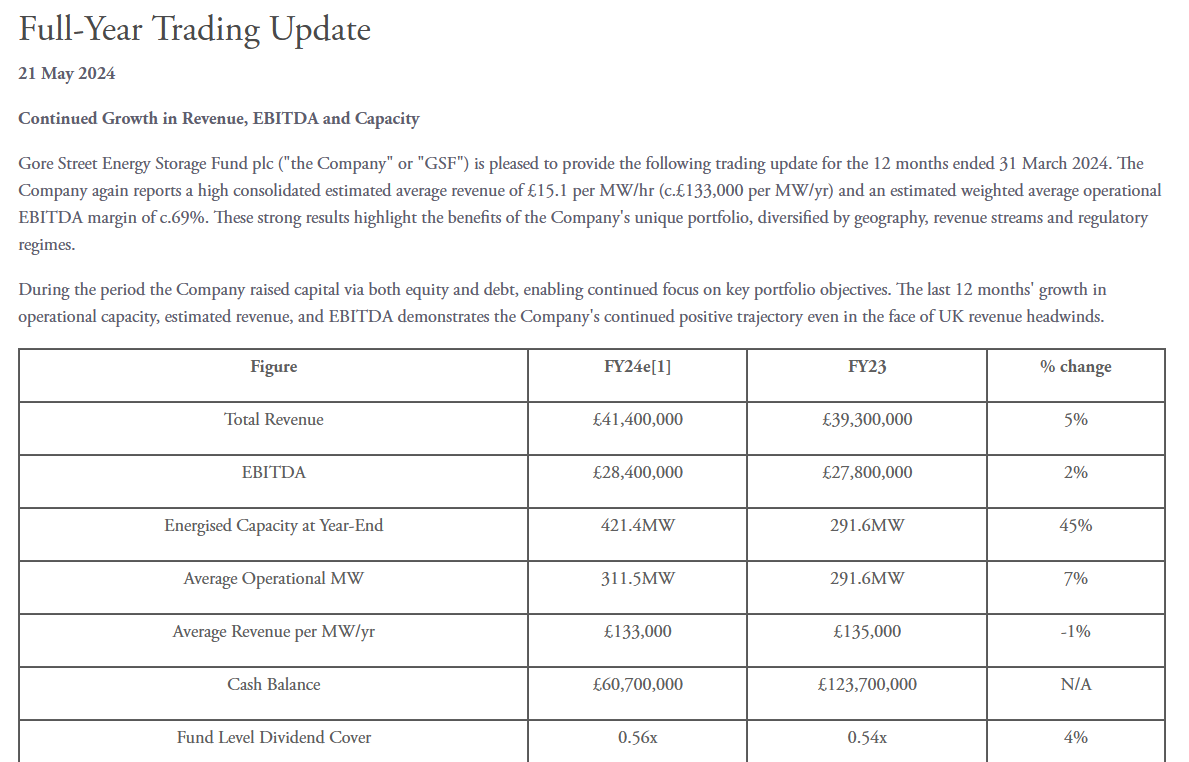

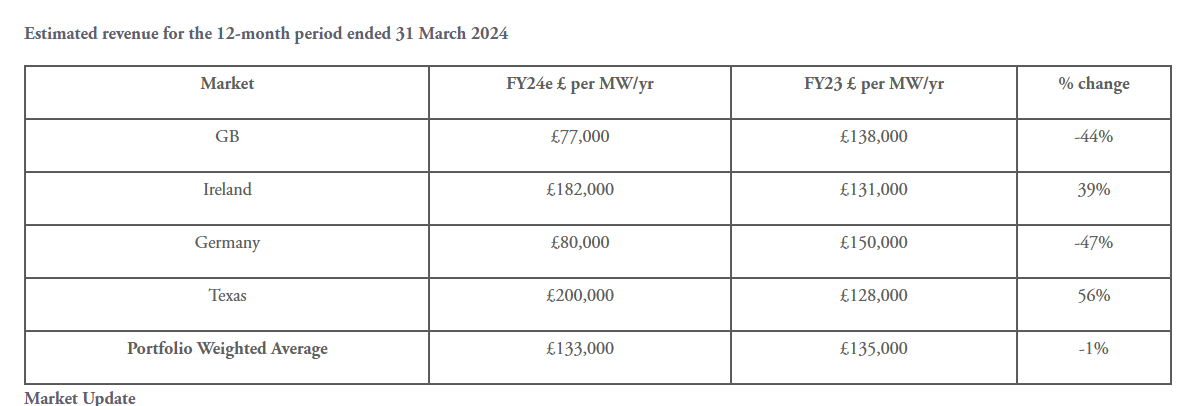

At a primary look, the Gore Road numbers appear to have held up lots higher than the Gresham ones:

The principle motive appears to be that they’ve diversified their portfolio throughout a number of jurisdictions, the place life appears to be (for now) extra snug for BESS house owners:

Learnings & Conclusion:

After the large Covid increase, the “New Power Infrastructure” pendulum clearly has swung again massively into the opposite course. The instance particularly of the Gresham Home fund exhibits that even BESS, at present nonetheless the most well liked subsector, has its points.

The comparability to the Gore Road fund nevertheless additionally exhibits that in such regulated markets, with massive dependencies on different gamers akin to grid operators and so forth., diversification throughout jurisdictions and markets can assist to mitigate particular person dangers.

The instance of the Gresham Home fund additionally exhibits that in such new areas, issues can flip shortly round. Particularly the BESS “arbitrage” enterprise mannequin may be very delicate to new capability. That is similar to funding methods that produce alpha for small quantities of cash after which the alpha disappears if many traders discover out about it.

So a primary mover benefit in that space can dissolve in a short time as organising and connecting BESS will not be rocket science, and battery costs are declining fairly considerably as of late.

To be sincere, I’m not 100% certain how these declining battery costs will influence current BESS belongings. Particularly as soon as, Sodium Ion batteries develop into commercially obtainable. Current BESS installations do have deliberate alternative cycles of one thing like 8-10 years, which ought to profit them. Then again, much more capability may hit the market.

For the UK, some quick time period aid is likely to be coming, however to me it’s not clear if and when. Nationwide Grid admitted in a latest FT article that their laptop techniques are certainly not succesful utilizing all of the obtainable BESS capability,

This primary take a look at the 2 funds didn’t yield any actionable perception. Going ahead, I’ll casually monitor each funds, nevertheless general I do suppose the Gore Road guys appear to be extra credible and appear to have the higher technique in comparison with the Gresham Home guys.

It additionally seems that the Gresham guys have been extra aggressive due to the pending sale of the fund supervisor itself.

General, the stand-alone BESS enterprise case appears to be fairly dangerous within the present atmosphere and must be rewarded by means of ample threat premia.